Every Company Will Be a Crypto Company

- Published on

- · 8 min read

Have thoughts on this topic? Join the conversation on X.

In 2022, I was working with fintech companies on banking as a service and embedded finance products. In the days and weeks following the FTX blowup, what struck me most was the schadenfreude that those around me expressed. People from the outside looking in were almost overjoyed that this industry they perceived to be a scam had finally collapsed.

At the same time, I was frustrated that these same people were doing little more than building UI wrappers to marginally extend the same traditional banking rails that had otherwise very little innovation.

However, working within fintech was also useful. After all, payments and financial services are also at the core of blockchains, and fintech shares the same goals of giving banking experiences to more people.

Why is this important? The crypto industry has spent years building financial infrastructure that now feels ready to transform global finance. We have fast L1s that can scale and $233B of stablecoins, but crypto feels largely confined to a self-referential ecosystem of existing, "native" users.

So...how can blockchains go mainstream? This article explores how the convergence of three elements...

- Stablecoins as the payment layer

- Blockchains as the new balance sheet

- zkTLS as the data bridge

...that will make every company a crypto company and in turn, bring crypto to the masses.

- Temperature check -- current sentiment

- The new balance sheet

- Consumer crypto

- zkTLS

1. Temperature check -- current sentiment

In September 2023, Matt Huang wrote an article called “The Casino on Mars”, where he gave a balanced take on how speculation is a powerful tool to drive real innovation. The casino acts as a trojan horse that introduces a new financial system.

A few months back, Jordi Alexander spoke (somewhat jokingly) on Steady Lads that inside the new financial system, there is simply another casino.

This exchange characterizes most of this cycle’s pessimism. Despite how far we’ve come with regards to regulation and institutional adoption, it sometimes feels like the industry also has not moved very far at all.

Since last cycle, countless teams have tried to define consumer crypto and make apps that real people might use. What exactly is the world where crypto powers the number one app on the app store? It's likely that we won't know until it happens, but we certainly are not there yet.

Admittedly, this persistent mental model that we must lure users into our casino and then trojan horse them with financial innovation has failed to deliver mainstream adoption.

2. The new balance sheet

Even though consumers seem to only onboard via pumpfun and new-wave casinos, the adoption story for businesses, enterprises, and institutions is very different.

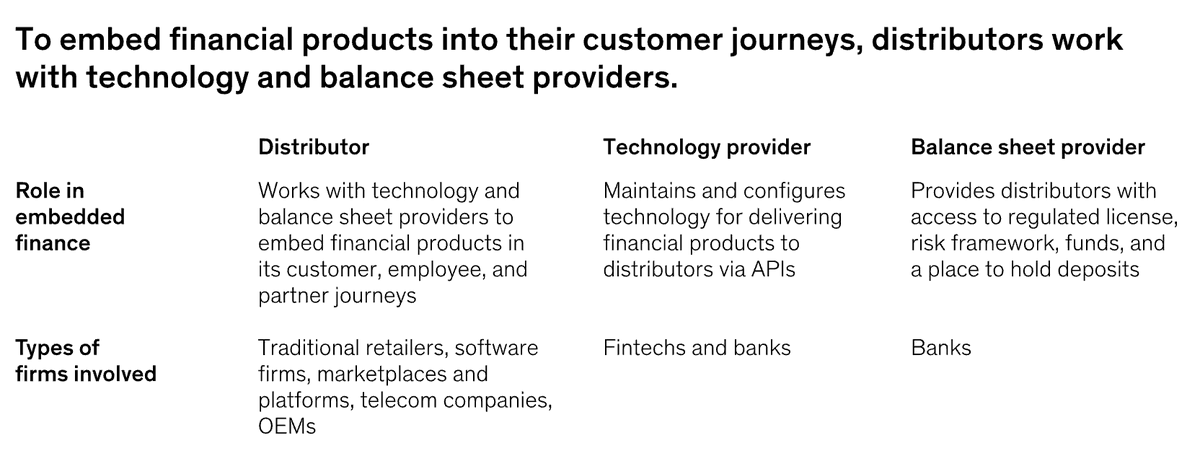

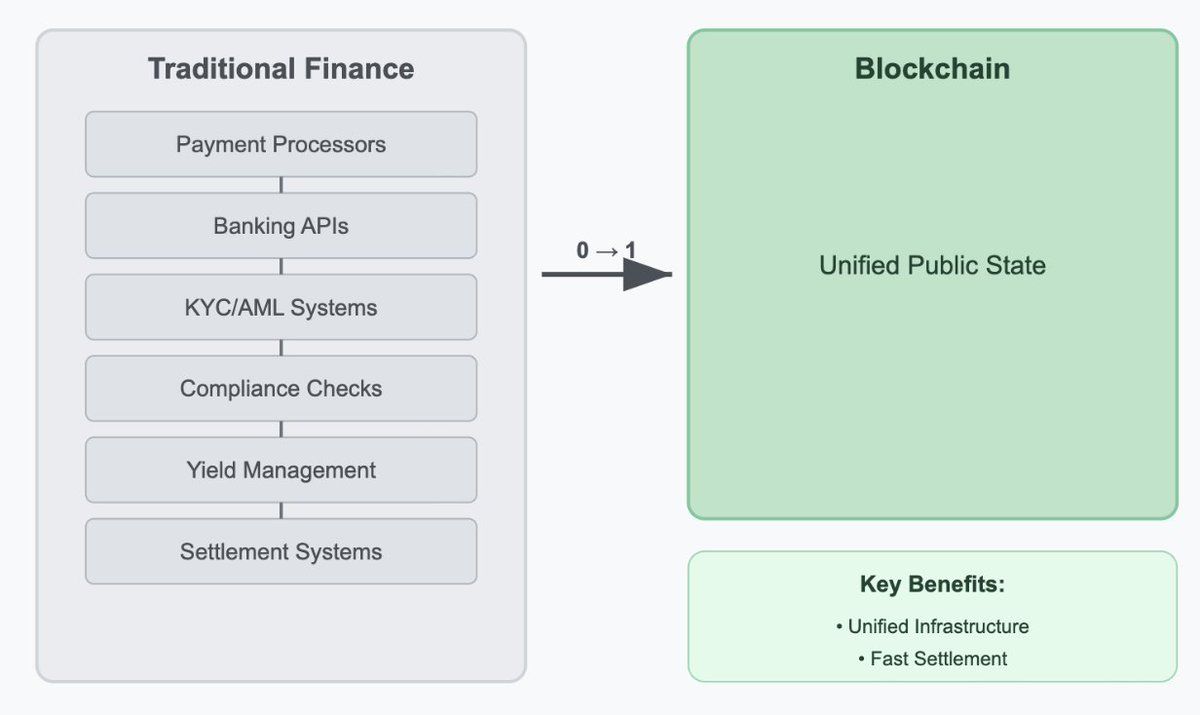

Traditionally, fintechs rely on banks as balance sheet providers. These days, companies can receive credit, deposit funds, and move money without ever touching a traditional banking interface. However, the back end for these products are always still banks - licensed or chartered financial institutions -- that act as balance sheet providers to offer these services.

Source: McKinsey on embedded finance

However, this story is starting to change. Stablecoins have proved to be the killer app for crypto, and large Web2 enterprises are adopting blockchains for payments, settlement, and transfers.

Whereas the stack to digitize banking is complex and relies on a myriad of APIs to rollup each layer as a service, blockchains already provide a unified public state that have fast, 24/7, global settlement.

Some examples:

- SpaceX: When SpaceX collects payments from Starlink customers in emerging markets, they convert these to stablecoins via Bridge so they do not have to deal with sending wires and taking foreign exchange risk

- Scale AI: Scale AI pays out contract workers who are part of a global network of data labelers via stablecoin rails

- Ramp: Ramp has pioneered stablecoins from an internal corporate treasury perspective. Theey've been one of the first non-crypto companies to deploy a meaningful allocation of their Corporate Treasury into USDC to capture traditional bond yield while maintaining high levels of liquidity

3. Consumer crypto

Ok, so now we've established that traditional businesses are using stablecoins and blockchains to manage their treasuries, pay out workers, and receive payments that all decrease cross-border frictions. While these use cases will continue to proliferate, there hasn't been any mainstream killer app beyond payments / stablecoins.

One of crypto's persistent challenges and perhaps fallacies has been the expectation that mainstream users would come to crypto platforms, rather than crypto capabilities coming to mainstream users.

Instead of enticing users with a casino and hoping to trojan horse them, what if crypto directly integrates into the existing behavior of crypto?

The path to scaling adoption thus far relies on a misunderstanding of how financial services have traditionally spread. The earliest forms of credit came through consumer companies themselves, where local shopkeepers and later department stores gave loans for regular consumers to buy groceries, equipment, or clothing.

So, if blockchains become the balance sheet for the next wave of user-facing financial products, who will be the distributors? And why would they choose to use these crypto rails?

Just as finance embeds financial products in non-financial customer experiences, I think crypto's path to mass adoption lies in embedding its capabilities into platforms people already use daily:

- Retail and e-commerce: Distribution channels for stablecoin payments and credit products

- Social media and content: Stablecoins for creator monetization, tipping, and subscription models

4. zkTLS

Although stablecoins already reduce cross-border payment friction, why else would users care? For those who do not already experience a need that stablecoins (productized US dollars) address, why would they onboard?

For those who do not feel the pain of traditional financial products, crypto needs to meet users where they are and provide a 10x better experience. Luckily, crypto's other use case is that it is fantastic at coordinating economic incentives and rewarding users via much richer data. However, in a Web2 world, how do companies get data that is both verifiable and private?

Enter...zkTLS.

Very simply, zkTLS is a bridge for Web2 data. zkTLS extends the standard TLS protocol (that secures all HTTPS connections) with cryptographic proofs:

- You visit a website through a secure TLS connection

- zkTLS generates a zero-knowledge proof that verifies specific data

- The proof reveals only what you choose to share, keeping everything else private

- Other applications can verify this proof to confirm the information is authentic.

While consumer applications may use blockchains + stablecoins for payments, to really onboard users they will need zkTLS for context and information.

While businesses will already be incentivized to adopt stablecoins from a cost perspective, they will need zkTLS to get deeper information about users and reward them to create cults.

Getting verified, private information about users from the apps they already use can turn every existing consumer company into a distribution channel for crypto. Instead of forcing users to come to crypto, have consumer companies reward users for engaging in their existing routines.

What makes zkTLS so transformative is its ability to unlock richer, more personalized experiences that were previously impossible. Traditional Web2 platforms operate in silos, unable to verify user information across different contexts without invasive data collection OR permissioned API creation between different parties.

Importantly, zkTLS fundamentally changes the way that consumer companies compete for users. Previously, platforms could only reward users for actions taken within their own ecosystem. With zkTLS, they can recognize and reward value from any part of a user's digital life. This exponentially expands the possibilities for customer acquisition.

We're seeing this in action already. Click in below for a great list of examples:

One use case I think of a lot is @earnos_io. Via @OpacityNetwork, EarnOS addresses the Proof of Humanity problem with internet advertising. As more of the internet is filled with fraudulent bot activity, the current cost per click model of companies and advertisers has similarly started to break.

How do consumer companies acquire customers in this new world? zkTLS gives Web2 companies deeper information from any other Web2 platform. Stablecoins provide the rails to reward individuals based on this information.

This is the way every company becomes a crypto company. Blockchains as core financial infrastructure represent an easy margin improvement opportunity for customers. But they can also provide the ability for growth and new customer interaction that has never existed before.