Ideas for Next Generation CLOB DEXes

fishmarketacad

@FishMarketAcad (opens in new tab)- Published on

- · 48 min read

Have thoughts on this topic? Join the conversation on X.

Centralized Limit Order Books (CLOBs) are the talk of the town in DeFi these days as traders demand the precision, low slippage, and familiar experience of centralized exchanges.

Yet, today's onchain CLOB-based spot DEXs still struggle with the same old problems of:

- Fragmented liquidity

- Inefficient capital usage

- Idle assets

I worked at one of the first fully onchain hybrid orderbook DEX for 4 years during which I had some thoughts about how CLOBs can be improved. I believe the next generation of DEXes won't just replicate CEX features onchain; they will innovate beyond them.

This article explores three innovative features, that I believe can tackle the above problems and transform CLOBs into a superior trading primitive:

- Omni Orderbook (aka Omnibook)

- Parallelized Liquidity Orderbook (aka PLOB)

- Integrated Lending and Borrowing

Although these are 3 separate ideas, they are not mutually exclusive as they are separate layers tackling different problems, and can in fact be built into a singular insanely powerful DEX.

Lets take a look how these concepts work, and of course why a high-performance, parallelized EVM like Monad is uniquely positioned to bring these ideas to life.

- 1. The Omnibook: A Unified Liquidity Layer

- Its own hybrid orderbook:

- How building on Monad solves this trade-off

- Onchain Liquidity: Tapping on the DeFi ecosystem

- How Monad Makes Onchain Aggregation Safer and More Efficient

- Integrating CEX liquidity: Accessing Unrivaled Depth

- How Monad Makes the Broker Model Viable

- Intent-based systems: Unified Gateway

- How Monad Makes This Vision Possible

- Omnibook Takeaway: A Unified and User-Centric Future

- 2. Parallelized Liquidity Orderbook (PLOB): Supercharged Capital Efficiency

- 3. Integrated Lending & Borrowing: Making Idle Capital Work

- Conclusion: The Blueprint for a Billion-Dollar DEX

1. The Omnibook: A Unified Liquidity Layer

Any sizeable market buy on a standalone DEX could incur significant slippage. A DEX with an Omnibook feature, however, could intelligently split and route that order across multiple venues for optimal execution. Its core is a sophisticated matching engine which display aggregated liquidity in real time, all executed atomically via smart contracts.

This concept of smart routing is already being pioneered on Monad by teams like @CloberDex, who have built the first meta-aggregator on the network.

The Omnibook vision takes this one crucial step further: what if, instead of this aggregated liquidity being a "black box," it were fully visualized on a single, unified order book? And what if aggregated more than just onchain AMM liquidity?

The Omnibook is a feature that aggregates liquidity from all available sources, such as but not exclusive to:

- Its own hybrid orderbook

- Onchain Liquidity

- CEXs

- Intent-based systems

The above liquidity sources and more can be combined into a single, unified orderbook interface to offer traders deeper markets and tighter spreads.

Let's go through them in depth (so devs can feel inspired):

Its own hybrid orderbook:

The DEX's native order book is its foundation. A modern CLOB shouldn't force a one-size-fits-all approach. A hybrid orderbook caters to both sophisticated market makers who require precision with limit orders and passive liquidity providers who prefer a simpler, set-and-forget experience.

This is what @KuruExchange has already achieved on Monad btw!

This is not limited to spot DEXes, @DrakeExchange which is a perp DEX natively built on Monad also feature a hybrid orderbook with liquidity vaults!

This hybrid model combines a standard limit order book with integrated AMM-style liquidity vaults.

- For Active Traders & Market Makers: They can place limit orders, post-quote, and run complex algorithms directly on the CLOB, just as they would on a CEX.

- For Passive Liquidity Providers: They can deposit assets into an automated market making (AMM) vault. This vault then takes their pooled capital and automatically provides liquidity on the order book on their behalf, earning them trading fees, just like on Uniswap.

How do these vaults work?

Instead of existing as a separate entity, the vault is tightly integrated with the order book. It algorithmically translates a passive liquidity position, often based on a familiar curve like Uniswap v2's x*y=k model, Uniswap v3 concentrated ranges, or even Kyberswap's amplification factor for 1:1 pegged assets (not yield-bearing), into a series of discrete limit orders on the CLOB.

Think of it like turning a smooth ramp (an AMM curve) into a very fine staircase (a series of limit orders).

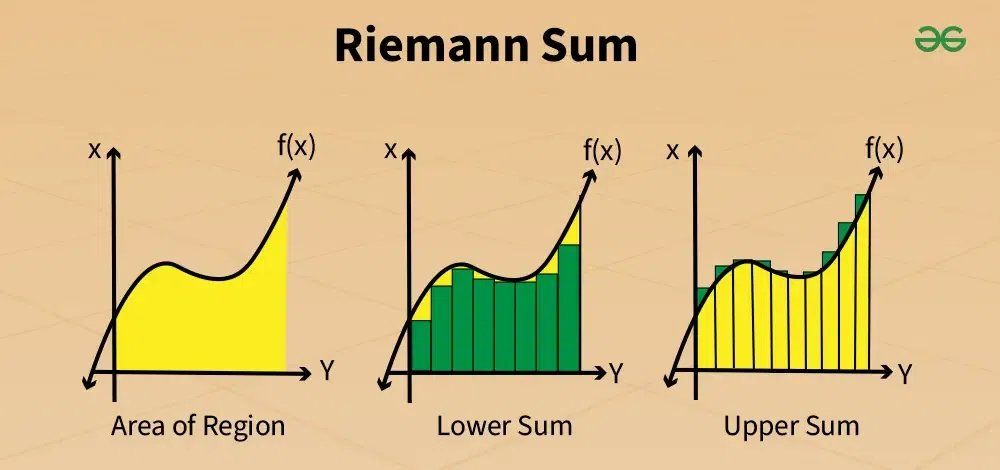

This process is conceptually similar to a core principle in calculus: approximating a continuous function with discrete steps. In calculus, you use integration (specifically, a Riemann sum) to find the area under a curve by summing up the areas of countless tiny rectangles.

Comparing parallels:

- The width of the rectangles (Δx) in the Riemann sum is analogous to the price tick size on the order book (e.g., $0.01, or 1 BPS). This is the discrete step along the price axis.

- The height of the rectangles (f(x)) is analogous to the liquidity depth (order size) placed at that specific price tick.

- The total area (the integral) that the Riemann sum approximates is analogous to the total liquidity available across a price range.

Source: https://media.geeksforgeeks.org/wp-content/uploads/20240611190455/Riemann-Sum.webp

This means that the thinner the rectangles, the smaller the tick size, and would allow AMM liquidity to feel more like a top-tier centralized exchange:

- Tighter Spreads: Market makers can place bids and asks incredibly close to the true market price, minimizing the bid-ask spread. This directly benefits traders, who lose less money on every swap.

- More Accurate Pricing: The price of an asset can reflect market sentiment with much higher fidelity.

- Fairer Execution for LPs: The AMM vault's behavior more faithfully mirrors the pure mathematical curve it's supposed to follow. There are fewer "gaps" in its pricing, reducing the risk of being picked off by arbitrageurs exploiting imprecise pricing.

So why not just make tick sizes very thin? There's a drawback: Everytime you halve the tick size, you double the number of price points within any given range.

For an AMM vault trying to "integrate" (pun very intended) its curve onto an order book, this is not a linear problem; it's an exponential one. The drawbacks are severe:

- Massive Computational & State Overhead: If a vault needs to place an order at every tick, halving the tick size means it now has to manage twice as many orders. Furthermore, when the market price moves, the vault orders are filled, and the vault's internal "price" shifts, it must then adjust its orders, cancelling and replacing potentially thousands of them to recenter the liquidity, including logic for handling partial fills. This creates a huge computational burden. The sheer number of orders also bloats the blockchain's state.

- Prohibitive Gas Costs: Every single one of those actions (placing an order, canceling an order, etc) is a transaction that costs gas. On a chain like Ethereum, the gas fees for a vault to constantly maintain thousands of discrete orders would be astronomical. It would become economically impossible for the vault to operate, as the operational costs would far exceed any trading fees earned by LPs. This is the primary reason why fully onchain, granular limit order books have struggled to gain traction on slower chains.

- High Latency & LP Risk: On a sequential blockchain, processing thousands of transactions takes time. If the vault's order updates lag behind the real market price because the chain is congested, it becomes vulnerable. Arbitrage bots will spot the stale, mispriced orders and trade against them, draining value from the vault's LPs. The faster the market moves, the more the LPs lose.

You can have precision (small ticks) or you can have low cost and low latency, and you can't have both on a sequential chain.

How building on Monad solves this trade-off

This is where Monad's architecture fundamentally changes the equation. It directly attacks the drawbacks of high precision.

- Parallel Execution for Computation: Monad can process the thousands of "cancel and replace" order transactions from the vault in parallel. Since updating an order at price P doesn't conflict with updating an order at price P+tick, these operations are perfectly suited for parallelization. This drastically reduces the latency of liquidity updates, protecting LPs from arbitrage.

- High Throughput for Gas Costs: Monad's ability to process a massive number of transactions per second (10k TPS or 1B gas/second in mainnet) drives down the cost of each individual transaction. This makes it economically viable for a vault to manage a hyper-granular order book with CEX-level tick sizes, as the operational costs become trivial.

- State Access: The challenge of reading and writing thousands of order slots from storage is solved by MonadDb, a custom database designed for high-frequency, parallel reads.

- LP Risk: Monad's asynchronous execution and 1-second finality ensure these complex liquidity updates are not only processed quickly but are also finalized almost instantly. This drastically reduces the window for stale-price arbitrage, protecting the vault's LPs from risk.

In essence, Monad allows a DEX to break free from the precision-performance trade-off. It enables the creation of a hybrid order book that is both mathematically precise and economically sustainable, offering users the best of both worlds: the passive, easy experience of an AMM with the sharp, efficient execution of a professional trading venue.

Now that you have a better understanding of why hybrid orderbooks are a good source of liquidity, and why they are better on Monad, let's move to the next type of liquidity an Omnibook can source.

Onchain Liquidity: Tapping on the DeFi ecosystem

Beyond its own hybrid order book, the Omnibook's true power comes from its ability to act as a universal liquidity hub for the entire on-chain ecosystem. This means sourcing liquidity not just from its own vaults, but from every other major DeFi protocol running on the same chain, other CLOBs, AMMs, and even aggregators (not all of the above of course as it overlaps), and presenting it all in one unified interface.

Let's break down the sources and the ease of integrating them.

Ease of Integration

- Easiest: DEX Aggregators. If an orderbook DEX also has a simplified swap UI (without showing an orderbook), it can easily integrate an aggregator into its swap function. However we are talking about CLOBs, so if you were to display the aggregator's liquidity in real-time as a depth chart (like a full order book), then it arguably becomes the hardest and I will explain why in a second.

- Easy: Other On-Chain CLOBs. Integrating with other order book DEXes is the most straightforward "like-for-like" integration. The liquidity data is already in a discrete format (limit orders at specific price ticks). The primary task is to read the state of the external order book and map its price levels and depths onto the Omnibook's interface.

- Hard: Direct AMM Integration. Integrating directly with a single AMM like Uniswap is more complex. As we discussed, this requires the "Riemann sum" logic—constantly reading the AMM's internal state (its curve) and translating that continuous function into a series of discrete orders. While computationally intensive, the logic is self-contained and targets a single, well-defined protocol.

- Hardest: Real-Time Aggregated Depth. This is the meta-problem and by far the most complex integration. To display a live depth chart from an aggregator, the Omnibook must essentially perform the aggregator's job in real-time. This involves making numerous, computationally expensive calls to all underlying liquidity sources and reconstructing the aggregated depth chart from scratch within its own system. It inherits the complexity of all other integrations combined.

The Twin Challenges: Computation and Staleness

Successfully integrating these sources requires overcoming two massive hurdles: the computational cost of representation and the economic risk of stale data.

1. The Computational Cost (The "How" Problem) Translating a dozen AMM curves into a live order book is a monumental computational task. Is it truly feasible, even on a high-performance chain?

Yes, but it requires a strategic approach. Natively performing these calculations on Monad, while thousands of times cheaper than on a sequential chain, still incurs a non-zero cost. A forward-thinking DEX can approach this not as a technical blocker, but as a go-to-market strategy.

In its growth phase, the DEX can use its treasury to subsidize the gas costs of this aggregation. This turns a technical expense into a powerful user acquisition tool, offering traders an unparalleled view of total on-chain liquidity for free. As the DEX captures market share, a network effect emerges: high volume attracts more LPs to deploy capital natively into the DEX's own efficient hybrid vaults. Over time, the DEX's native liquidity becomes so deep that its reliance on expensive external aggregation diminishes, creating a sustainable, long-term competitive moat.

What about coprocessors? They can make this computationally cheaper, as the onchain task becomes verifying a proof of the AMM-to-order-book conversion. However, with current technology, they cannot provide the real-time, per-block updates (correct me if I am wrong). This latency can defeat a core purpose of a live exchange, which may be fine for non-urgent traders, however in that case, using an intent-based system would probably be a better approach.

2. The Stale Data Risk (The "When" Problem)

This is the more subtle but critical trade-off inherent in aggregating external liquidity in real-time. It's a Time-of-Check to Time-of-Use (TOCTOU) vulnerability, a classic race condition that sophisticated MEV bots can exploit.

Here's the walkthrough for a market order:

- Time of Check: In Block N, the Omnibook contract reads the price on an external Uniswap pool (e.g., 3,000 USDC/ETH).

- The Race: A MEV bot sees a user's trade targeting this price and front-runs the Omnibook by submitting its own transaction to the Uniswap pool first.

- Time of Use: The bot's transaction executes first, pushing the real Uniswap price to 3,001 USDC. The user's trade then executes at this slightly worse price.

For a professional trader, this 0.03% slippage is a loss. However, for a retail user making a smaller trade, the convenience of accessing deep liquidity might outweigh the minor price difference. This isn't necessarily a "problem" for everyone, but a known trade-off for accessing aggregated liquidity. The DEX's user interface should make this clear.

This vulnerability also affects limit orders, but in a different way. Instead of slippage, MEV bots that move prices can cause trades to fail entirely even if the price appears to hit the user's target, creating "phantom orders, price or liquidity" that erodes trust.

How Monad Makes Onchain Aggregation Safer and More Efficient

Monad's architecture is designed to defeat this stale data vulnerability.

- Shrinking the Arbitrage Window: Monad's 0.5 second block times are the primary defense. The time between the "check" and the "use" is compressed. This gives arbitrage bots a smaller window to detect an opportunity and submit a competing transaction. While not impossible to exploit, it becomes harder and less profitable.

- Efficiently Querying with Parallel Execution: An Omnibook needs to check the state of multiple external protocols to find the best price. On a sequential chain, this means querying Uniswap, then waiting for the result, then querying Curve. On Monad, these checks can be executed in parallel. The Omnibook can query every relevant on-chain liquidity source concurrently, getting a comprehensive view of the market almost instantly and with maximum efficiency.

- Reliable Composability: As a fully EVM-equivalent environment, integrating with any protocol ported from Ethereum is seamless. The Omnibook can reliably call and interact with other contracts, knowing the underlying execution environment is fast, cheap, and secure from the kinds of latency-based attacks that plague slower chains.

Integrating CEX liquidity: Accessing Unrivaled Depth

To truly compete, a DEX needs to tap into the deepest liquidity pools in crypto: centralized exchanges. The Omnibook can achieve this in a non-custodial way by using a network of independent intermediaries, or brokers.

When a user places a trade that is best routed to a CEX, a broker executes it on their behalf using their own pre-funded CEX account, with settlement occurring atomically onchain. The user's funds never leave their wallet until the trade is finalized, completely eliminating deposit risk.

Here's a simplified walkthrough of the atomic settlement process:

- Order & Lock: A user performs a taker order to purchase MON with USDC. The user's trade is routed to a broker. A smart contract on Monad locks the user's USDC.

- Offchain Execution: The broker's software detects the locked funds, a risk-free signal for them to proceed. They use their own capital to execute the corresponding buy order on the CEX.

- Onchain Fulfillment: The broker immediately withdraws the purchased asset (e.g., MON) from the CEX directly to the user's on-chain wallet.

- Release & Settle: The smart contract automatically detects the arrival of the MON in the user's wallet and releases the locked USDC to the broker, plus a small fee for their service.

The Challenges: Capital and Asset Availability

While elegant, this model presents two significant, real-world challenges that have prevented its widespread adoption:

- The Broker Capital Problem. Being a broker is capital-intensive. They need both a substantial stake to be trusted and significant working capital across multiple CEXs to fill orders. This high barrier to entry can lead to a centralized network of only a few large, well-capitalized brokers. However, as the Monad ecosystem matures, this could be mitigated. It's easy to imagine shared security protocols (like EigenLayer) deploying on Monad allowing brokers to use restaked assets to meet their capital stake requirements, significantly lowering their barrier to entry.

- 2. The CEX Asset Availability Problem. The broker model only works for assets that can be freely deposited and withdrawn between CEXs and the Monad chain, such as MON and USDC. This would limit the Omnibook's CEX integration to only those specific markets. This requires a business development effort to encourage CEXs to list more Monad-native assets or allow non-native assets to be deposited and withdrawn to and fro Monad. However, this challenge naturally resolves itself with ecosystem growth. As more high-quality applications launch their tokens on Monad and subsequently get listed on major CEXs, the number of markets that can benefit from deep CEX liquidity integration will organically expand over time.

- The Latency Risk Problem. This is the critical technical vulnerability that Monad solves directly. The broker is exposed to risk during the time gap between spending their own funds on the CEX and getting reimbursed by the on-chain contract. This "risk window" includes CEX withdrawal processing times and, most importantly, blockchain finality time.

How Monad Makes the Broker Model Viable

Monad's architecture is uniquely designed to solve the latency risk problem, which in turn makes the capital problem more manageable.

- Solving Latency Risk with 1-Second Finality: This is the single most important feature. Monad's 1-second finality shrinks the broker's on-chain risk window from many minutes to a single second. An irreversible settlement in one second is a tiny, acceptable business risk. This single feature transforms the broker model from a dangerous gamble into a safe, viable, and profitable enterprise.

- Making Capital More Efficient: By reducing risk and settlement time, Monad allows brokers to cycle their capital much faster. A broker can service hundreds or thousands of trades per day with the same pool of capital that might only service a few dozen on a slower chain. This can improve their profits and lower the barrier to entry, encouraging a more decentralized network of brokers to participate.

- Low-Cost Transactions: The settlement process is governed by a smart contract that ensures an atomic economic outcome, meaning the exchange is guaranteed to complete successfully for both parties, or not at all. Monad's low gas fees ensure that the cost of this trust-minimized interaction is negligible, allowing brokers to operate profitably even on small spreads.

Intent-based systems: Unified Gateway

The final layer of liquidity the Omnibook can tap into is the most forward-looking: intent-based systems.

Let's quickly understand intents with a real world analogy:

- Standard Transaction: You go to a restaurant, walk into the kitchen yourself (go onchain), and open your mouth to tell the chef exactly how to cook your meal (opening your mouth means you spend your own gas), and pay for it right there.

- Intent (Signed Message): You write a note that says, "I want steak for under $50, here's my credit card deets to prove I'll pay for it." You then give this note to a personal shopper (the solver). The shopper (who knows all the best butchers and may even have discount cards) goes out and finds the best possible steak, cooks it for you, and delivers it. You only pay when the final meal arrives, and the shopper handles all the intermediate steps.

Difference between onchain transactions and intents which are offchain:

- On-Chain Transaction: When you submit a standard transaction (like a swap on Uniswap), you are sending a command directly to the blockchain. You pay gas upfront, and the miners/validators are obligated to try to include and execute your command onchain.

- Off-Chain Signed Message: When you sign an intent, you are using your private key to create a piece of data that says, "I, wallet 0xabc..., authorize this specific outcome." This signed message is not submitted to the blockchain yourself. It's just a piece of data. It has no power on its own and costs you no gas to create. You then hand this signed message to a solver or an intent network who takes your authorized desire and build an actual, executable onchain transaction around it. The solver will then be the one to pay the gas and submit this final transaction.

If you want to learn more, I wrote a quick explainer about intents recently:

The Challenge: A Fragmented User Experience

The world of intents, with its RFQ systems and solvers, has traditionally existed in a separate universe from the world of onchain CLOBs. Users are forced to choose: "Do I want the precise, transparent experience of a CLOB, or do I want the potentially better pricing of a 'black box' intent system?" This fragmentation creates a confusing and inefficient user decision experience.

The Solution: Every Order is also an Intent

A next-generation DEX can adopt a powerful, parallel approach. Every single order placed on the Omnibook is simultaneously treated as two things:

- An order on the native onchain CLOB.

- An open intent broadcast to the solver network.

The system then operates on a "best-of-both-worlds" principle. When an order is placed, the DEX initiates a very short auction period (e.g., the duration of a single Monad block). During this window, solvers can compete to beat the price available on the native CLOB. The user is guaranteed to get the best possible execution from either the on-chain book or an off-chain solver, whichever is superior.

The Value-Add: Why This Is a Game-Changer

This model is a significant value add because it elevates the DEX from a simple trading venue to a universal intent platform.

- Guaranteed Best Price: Traders no longer need to choose between different systems. They interact with a single, deep order book that seamlessly represents liquidity from every source—native market makers, AMMs, and the vast, off-chain world of intents.

- Creating a Liquidity Super-Layer: This creates a powerful network effect. Native CLOB liquidity can now interact with intent-based liquidity. A limit order placed on the book can be filled by a solver fulfilling an offchain intent, and vice-versa. The entire system becomes more liquid and efficient than the sum of its parts.

- Future-Proofing with "Intent Signalling": This is the most profound benefit. The platform is no longer limited to simple swaps. It can become a hub for expressing any complex financial desire. There would have to be a new UIUX to make these orders easier to create but what it unlocks is worth it imo. A user could submit an intent to execute txs like: "Execute a TWAP (Time-Weighted Average Price) order to buy 100 ETH over the next hour." "When my yield farm rewards reach $50, claim them and reinvest." "Sell my ETH only if the gas price is below a certain threshold."

Additionally, this doesn't have to be limited to a single chain. The final frontier for this technology is to abstract away the blockchain itself. This is the vision where protocols like Aori are innovating. By combining a universal intent-based system with cross-chain messaging layers like LayerZero, they aim to turn the DEX into a seamless portal to any token on any chain.

Imagine the user experience: A user on the Monad-based DEX could submit an intent to swap their USDC for a niche token that only exists on Solana. An off-chain solver would accept this intent, handle all the complex bridging and swapping in the background, and deliver the final Solana-based tokens back to the user's specified address. The user only has to sign a single message to express their desire.

For such a system, Monad serves as the ideal "home base", an ultra-performant, low-cost settlement and asset management hub from which users can safely and efficiently interact with the entire multi-chain world. This transforms the DEX from the center of one ecosystem into a true gateway to all of crypto.

The Trade-offs and User Choice

This powerful model does have trade-offs. It introduces a slight execution delay (up to one block, or ~1 second on Monad) for marketable orders as the system waits for solver bids. While this is negligible for most users, especially in exchange for a better price, it might not be suitable for all high-frequency strategies.

This is where the ultimate user experience comes in. The Omnibook can offer this as a user-configurable setting. A trader could choose:

- "Optimize for Best Price" Mode (Default): Broadcasts their order as an intent to get the best possible execution.

- "Native Only" Mode: Submits their order exclusively to the on-chain CLOB, opting out of the intent system for the most direct, albeit potentially less price-optimized, execution path.

How Monad Makes This Vision Possible

This grand vision of a universal intent hub places an immense data processing burden on the underlying chain.

- Handling the Data Firehose: The platform must process a constant stream of simple quotes, complex structured intents, and solver solutions. Monad's parallel execution and MonadDb are essential for managing this information pipeline without clogging the network.

- Enabling Complex Settlement: A solver fulfilling a multi-step conditional intent will generate a very complex transaction. Monad's high gas limits and performance ensure these sophisticated transactions can actually be settled on-chain without failing. This robust settlement layer gives solvers the confidence to build and offer more advanced products.

- Solving the 'Black Box' with Credible Neutrality:" The biggest risk in many intent systems is the reliance on a centralized sequencer or builder who can censor or front-run users. Monad's globally distributed validator set provides credible neutrality. Because there is no single, dominant entity controlling block production, it becomes harder for any one party to manipulate the flow of intents. This fosters a truly fair and open marketplace for solvers, which directly translates to better, more reliable outcomes for users.

Omnibook Takeaway: A Unified and User-Centric Future

The Omnibook is more than just a feature; it's a fundamental reimagining of what a DEX can be. By acting as a universal liquidity hub, it solves the core problem of fragmentation that plagues DeFi today.

Let's recap the layers of liquidity it can integrate:

- A Native Hybrid Orderbook: Combining the precision of a CLOB with the simplicity of AMM vaults

- On-Chain Liquidity: Safely tapping into other on-chain protocols like AMMs by leveraging Monad's high performance and low latency

- CEX Liquidity: Tap on CEX liquidity via non-custodial brokers

- Intent-Based Systems: Allow users to place orders which are broadcasted as intents in parallel to receive the best possible price from a competitive solver network

Ultimately, the Omnibook's complexity is orchestrated to create a simple, powerful, and user-centric experience. The final piece of the puzzle is the user interface. Through a simple series of toggles, traders can customize their experience based on their own unique needs and risk tolerance.

Imagine an interface where a trader can choose:

- Native Liquidity: The fastest, most direct execution path.

- On-Chain Aggregation: Access deeper liquidity from other AMMs, understanding the minor risk of data staleness.

- CEX Broker Network: Tap into centralized exchange depth for large orders.

- Intent-Based Optimization: Broadcast their order to solvers to find the absolute best price, accepting a one-second delay for optimization.

This is the end-game: a DEX that doesn't force a single model on its users, but provides a comprehensive suite of tools and empowers them with the choice to build their own perfect trading experience.

After aggregating all the liquidity, let's explore how a DEX can make sure of that liquidity more efficiently by looking at PLOBs.

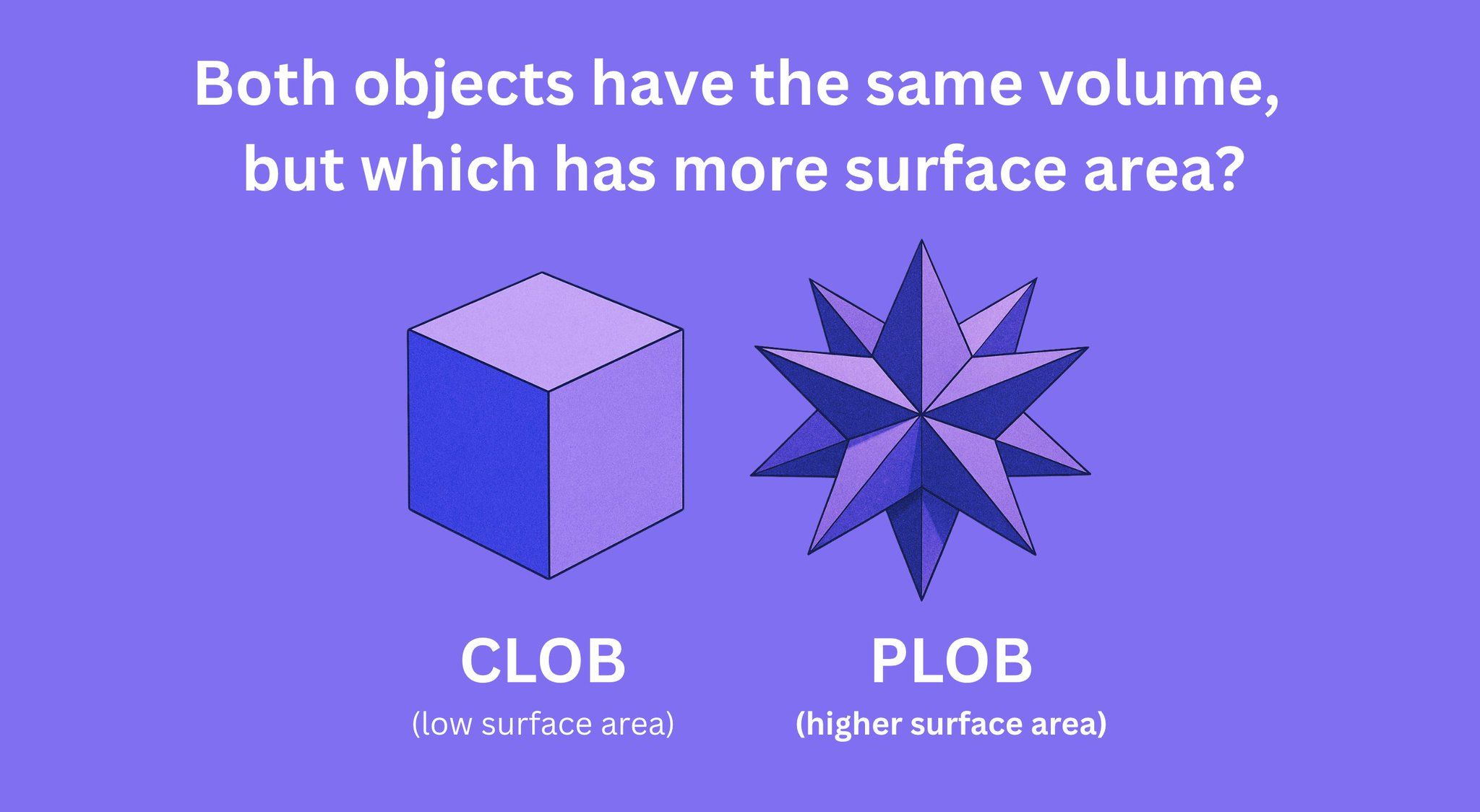

2. Parallelized Liquidity Orderbook (PLOB): Supercharged Capital Efficiency

A traditional CLOB is like a cube: its capital (volume) is confined to a single market (low surface area).

A PLOB is like a star: the same capital is projected across hundreds of markets, massively increasing its 'surface area' for earning fees.

Volume = TVL

Surface area = Market Exposure / Fee generating opportunities

While the Omnibook focuses on aggregating external liquidity, the Parallelized Liquidity Orderbook (PLOB) revolutionizes how a DEX utilizes its own internal, native liquidity. It is a paradigm shift in capital efficiency, moving from isolated liquidity pools to a unified, shared liquidity model.

The Core Concept: Limited Liquidity Pool for Unlimited Market Exposure

Let's use an analogy to explain the difference between a CLOB and a PLOB.

CLOB: Like having a separate bank account for every bill.

You have one bank account strictly for your rent, another for your electricity bill, and a third for groceries. To pay your rent, you have to make sure there's enough money in that specific account. If your grocery account has extra cash, it can't help you pay your rent. You are constantly moving money between accounts when you need the liquidity.

PLOB: Like having a single account with smart software to handle bills.

You have all your money in one central account. Your budgeting software (the PLOB logic) knows your upcoming bills (your resting limit orders across all markets). It reserves the funds mentally, but the money is never truly locked. If an unexpected expense (a filled trade) comes up, the money is taken from the central pool, and the software instantly recalculates what's left for all other upcoming bills, "cancelling" any you can no longer afford.

This concept is powerful for spot markets and becomes a true game-changer for perpetuals.

Shoutout to @0xceleris for being the first PLOB DEX I know building this.

Still confused? Let's go through some concrete examples.

PLOB for Spot Markets

In a traditional spot AMM, if you want to provide liquidity for MON/USDC and MON/ETH, you need to deposit capital into two separate pools. This is capital intensive.

The PLOB model shatters this limitation. In a PLOB DEX, an LP can deposit a single asset, for example, MON, into a master PLOB vault contract and then specify which markets they want this single pool of capital to be "replicated" or "parallelized" onto.

The PLOB system then takes their single-sided MON deposit and algorithmically represents it as orderbook liquidity across all their chosen markets simultaneously.

This means a single $10,000 deposit of MON can be used to provide sell-side liquidity on the MON/USDC, MON/ETH, and MON/SOL order books all at the same time.

This dramatically increases the "surface area" for capital utilization. The LP's MON is no longer waiting for volatility in just one market; it's actively providing liquidity and earning fees from the volatility of multiple markets at once.

This increased fee generation does come with a trade-off. By being exposed to multiple pairs, the LP's capital is also exposed to impermanent loss (IL) from multiple vectors. However, for an LP who is long-term bullish on the base asset (MON in this case), the increased fee revenue can potentially outweigh the risks of IL, making it a highly attractive strategy.

Example 1: Parallelizing Liquidity

Let's walk through a detailed example. Assume MON is trading at $1.00.

- Alice's Deposit: Alice deposits 1,000 MON into a PLOB vault. She wants to provide liquidity for both MON-USDC and MON-ETH markets.

- Projection: The PLOB system, using the "AMM-to-order-book" visualization we discussed earlier, projects her liquidity onto two markets: On the MON/USDC order book, a "sell wall" of her 1,000 MON appears as a series of limit sell orders, perhaps concentrated in a range from $1.00 to $1.05. On the MON/ETH order book, another sell wall of the same 1,000 MON appears, priced near the current MON/ETH exchange rate. Alice is now providing deep, sell-side liquidity on two major pairs using a single source of capital. And this can be extending to Nth markets.

Example 2: The Atomic Cascade on a Fill

This is where the magic happens. A second later, the market moves.

- The Fill: A large buyer on the MON/USDC market pushes the price up, and a trade executes against Alice's liquidity range. 500 of her MON are swapped for 510 USDC.

- The Master Account Update: Alice's master vault state is now: 500 MON and 510 USDC.

- The Atomic Cascade: Because she now only has 500 MON available to sell, the system must atomically (within the same transaction) update her liquidity on all other linked markets. The sell wall she was providing on the MON/ETH order book is instantly and automatically reduced by 500 MON. This prevents the system from ever promising liquidity that has already been sold. If the price of MON later drops against USDC and her 510 USDC is swapped back into ~500 MON, her liquidity on the MON/ETH market is atomically restored.

The complexity of a PLOB system in spot markets grows with the number of quote assets involved. Tracking the value and state of an LP's holdings across MON, USDC, ETH, and SOL simultaneously is a significant challenge.

The model becomes far more seamless and powerful when applied to an environment that uses a single, unified denomination for margin and settlement, such as perpetual markets.

PLOB for Perpetual Markets

In the world of perpetuals, where all profits, losses, and collateral are typically denominated in a single stablecoin (like USDC), the PLOB model can be implemented in its purest and most powerful form. Here, a user's margin is not just capital; it is a universal key that unlocks exposure across the entire platform.

In a PLOB-based perp DEX, a user's margin is not locked to a single position or order. Instead, their entire account margin acts as a single, shared pool of collateral that can back resting limit orders and open positions across all markets simultaneously.

Let's explore this with two critical examples.

Example 1: The Trader's Perspective (The "Stink Bidder")

Imagine a trader who loves to place "stink bids" and "out-of-the-money asks" to catch wicks during volatile moves.

- The Setup: A trader has $1,000 in their margin account. BTC is trading at $100k, and ETH is at $3k.

- The PLOB Advantage: The trader can use their single $1,000 margin pool to place multiple resting limit orders simultaneously: A limit long order for BTC at $90,000. A limit short order for BTC at $110,000. A limit long order for ETH at $2,500. A limit short order for ETH at $3,500.

- The Atomic Fill: If a sudden market dump (like tariffs or war fears) causes the ETH price to dump to $2,500, their ETH long order is filled. The margin required for this new open position is now consumed from their total account. Instantly, and in the same atomic transaction, the system recalculates their remaining available margin. If the remaining margin is no longer sufficient to back their resting BTC or SOL orders, those orders are automatically cancelled, preventing any risk of liquidation.

This allows a trader to maximize their exposure to market opportunities without needing to fragment their capital into tiny pieces for each potential trade.

Example 2: The Vault's Perspective (An Ultra Liquid Perp DEX)

This is where the PLOB model truly shines. Consider a perp DEX with a single liquidity vault (like Hyperliquid's HLP) that acts as liquidity to traders.

- The Setup: A DEX has 100 markets but only $1 million in its LP vault. In a traditional model, this would mean an average of only $10,000 of liquidity depth per market, which is incredibly thin.

- The PLOB Advantage: The PLOB allows the vault to project its entire $1 million of liquidity depth onto all 100 markets simultaneously on both sides. The order book for every single market, from BTC to the newest memecoin that just got listed, can appear deep and full.

- The Benefit: This dramatically increases the "surface area" for the vault's capital to be utilized. Instead of earning fees on just a few active markets, the vault earns fees from trades across the entire platform.

- The Rebalancing: As traders take one side of the market (e.g., going long on BTC), the vault's exposure shifts. The vault can algorithmically factor this into its quoting strategy to create a funding rate skew, which incentivizes arbitrageurs to take the other side, freeing up the vault's capital and rebalancing its delta exposure risk.

This vault benefit can also be extended to user created vaults, allowing independent traders to be more capital efficient with the capital they receive (or get rekt faster lol).

This has profound benefits:

- Radical Capital Efficiency: Traders and market makers can provide liquidity across dozens of markets simultaneously with the same pool of capital, drastically increasing their potential exposure and fee generation.

- Instant Liquidity for New Markets: A DEX can list a new token pair or perp market and have a deep, liquid order book from day one, as LPs can provide liquidity without needing to fragment their capital.

- Dynamic Market Making: Liquidity vaults can deploy sophisticated strategies, dynamically adjusting quotes and spreads across all markets in response to their real-time risk exposure (vol, gamma, delta, etc).

A PLOB-based perp DEX can therefore offer a hyper liquid (pun intended again) trading experience compared to a competitor with 100x the TVL.

The Challenge: State Synchronization

The complexity of tracking a single margin pool's real-time exposure across hundreds of markets and instantly recalculating and cancelling orders is computationally immense. This is the exact "state synchronization nightmare" we discussed in the spot section, but amplified.

This is a problem that feels tailor-made for Monad. Parallel execution is essential to handle the atomic cascade of order cancellations across multiple markets after a single fill. The high throughput and low gas fees make the constant stream of order management economically viable. MonadDb provides the fast, parallel state access needed to read the master margin account and all linked order books simultaneously.

The PLOB model, for both spot and perpetuals, represents a leap in on-chain efficiency that is only practical in a high-performance, parallelized environment.

How a PLOB could be done and how Monad makes it practical

A key question is how a system can manage this complex, interconnected state. One approach is a modular "hub-and-spoke" architecture.

- The Hub: A single Master Account contract acts as the core. Its only jobs are to hold the user's master collateral (whether it's spot assets or margin) and to process the final, settled state changes.

- The Spokes: For each market (e.g., MON/USDC or MON-PERP), a separate, lightweight Market Logic contract is deployed. This "spoke" reads the available capital from the hub and is responsible for placing and managing the orders on its specific market.

When a trade is filled on one spoke (eg in the BTC-PERP market), it reports the change back to the hub. The hub updates the master account's state, and all other spoke contracts automatically read this new state and adjust their own orders accordingly. This modular design enhances security, simplifies upgrades, and naturally aligns with Monad's parallel architecture, making the entire system more robust and efficient.

The PLOB model is like a poster child for the benefits of Monad's parallelized architecture.

- Parallel Execution Solves the Cascade: After the initial trade updates the LP's master account (a sequential step), the subsequent updates to all other linked order books are perfectly suited for parallelization. Monad can process the cancellation and replacement of orders on the MON/ETH and MON/SOL and MON/Nth order books concurrently, turning a complex bottleneck into a manageable, high-speed operation.

- High Throughput & MonadDb: Monad's enormous gas capacity makes the cost of these multiple state updates affordable, while MonadDb's ability to handle parallel database reads allows the system to efficiently check the state of the master vault and all satellite order books at once.

The PLOB transforms passive LP capital into a dynamic, hyper-efficient engine for market-making, a vision only made possible by a high-performance, parallelized environment.

PLOB Takeaway: The strongest possible native liquidity foundation

A DEX that is both a PLOB and an Omnibook creates a powerful, self-reinforcing loop:

- A Deeper "Last Resort": The PLOB ensures that the DEX's own native order book is incredibly deep and efficient. This means the Omnibook's smart router has a fantastic "default" option. If it can't find a better price externally, it can always fall back on its own ultra-efficient native market. This makes the entire DEX more robust.

- Better Pricing for Solvers: When the DEX broadcasts an intent to the solver network, solvers can use the DEX's own deep, PLOB-powered native liquidity as a source to help fill the order. A solver might fill 70% of an order from a private source and the final 30% from the DEX's own book. The PLOB makes the DEX a more attractive partner for the entire solver ecosystem.

- The Ultimate User Experience: A user doesn't need to know or care where the liquidity comes from and whether it's real or virtual. They just see one, insanely deep order book. When they place a market order, the Omnibook's router finds the best price, whether it's from an external AMM or from an internal PLOB vault. When they become an LP, the PLOB allows them to provide liquidity to the entire DEX ecosystem with a single deposit.

The PLOB creates the strongest possible native liquidity foundation, and the Omnibook builds on top of that foundation by connecting it to the entire universe of external liquidity.

A DEX with just one of these features is innovative. A DEX with both is a true category killer. But we are not done yet. What if you could make the existing idle liquidity work even harder to generate more yield?

3. Integrated Lending & Borrowing: Making Idle Capital Work

The third and final innovation is to break down the wall between trading and lending. A truly next-generation DEX can vertically integrate its own lending market, creating a Shared Liquidity Pool where the same pool of assets can be used for swaps, leveraged trading, and borrowing simultaneously. This supercharges capital efficiency and unlocks novel financial primitives.

The Core Idea: Making Every Asset Productive

In this model, any idle liquidity within the DEX—whether it's an LP's assets sitting out-of-range in a concentrated liquidity vault or the margin collateral backing a trader's position—is automatically deposited into the DEX's native lending market to earn yield.

Let's explore simple and powerful use cases this unlocks.

Simple use cases

Example 1: The Yield-Enhanced LP

- The Setup: Alice provides liquidity to a MON/USDC concentrated liquidity vault in a range between $0.95 and $1.05. The current price of MON is $1.00. Her liquidity is active.

- The Innovation: The market moves, and MON rises to $1.10. Alice's position is now entirely in USDC, and her capital sits idle, out-of-range, earning zero trading fees. In a traditional DEX, this is dead capital waiting to re-enter the range, unless Alice rebalances it manually.

- The Integrated DEX: The system automatically detects that her USDC is idle and deposits it into the native lending pool. Alice immediately starts earning a variable lending APR on her capital, even while her LP position remains open. If the price of MON drops back into her range, the USDC is atomically withdrawn from the lending pool and made available for trading again, seamlessly and without any action required from her.

Example 2: The Capital-Efficient Leveraged Trader

- The Setup: Bob wants to open a 5x leveraged long position on ETH. He deposits $1,000 USDC as margin.

- The Integrated DEX: The protocol borrows $4,000 worth of ETH from the Shared Liquidity Pool to create his position. But crucially, Bob's own $1,000 USDC margin collateral isn't just sitting there. It is also automatically deposited into the lending pool, where it starts earning him passive interest.

- The Benefit: Bob is both in a leveraged trade and earning yield on his underlying collateral. This "dual-use" of assets dramatically improves capital efficiency for traders.

With this feature, traders can opt-in to have the capital backing their resting limit orders automatically deposited into its own lending markets, or even external lending markets or vaults (eg Aave).

When a taker's order matches the resting limit order, the system performs an atomic withdrawal and swap: it instantly pulls the required capital from the yield vault and executes the trade in a single, seamless transaction. The trader earns yield on their liquidity right up to the moment it's used.

This transforms a standard CLOB into a dynamic, yield-bearing instrument, creating a powerful incentive for market makers and traders to place more limit orders and deepen the book's liquidity.

New Primitive #1: Liquidation-Free Leverage

This deep integration allows for entirely new financial products. Imagine a way to get leverage without liquidation. This is done by allowing traders to borrow liquidity for a fixed duration directly from the idle liquidity sitting at specific future price ticks of an AMM pool.

- The Setup: A trader wants leveraged long exposure to ETH. The current price is $3,000 (let's call this Tick 50). An LP has provided a large amount of ETH liquidity concentrated at Tick 60, which corresponds to a future price of $3,100. This ETH is an idle asset, committed but not yet active.

- The "Tick Borrow": The protocol allows the trader to pay a small, upfront fee to the LP at Tick 60. In exchange, they receive the right to use (borrow) that ETH for a fixed period (eg one hour).

This mechanism's payoff is better understood through an actual options trade: the story of Thales and the olive presses.

- The LPs are the owners of the olive presses (the idle ETH).

- The Trader is Thales, who believes the demand of olive (ETH price) will go up and wants leveraged exposure.

- The "Tick Borrow" Fee is the deposit Thales paid to the olive press owners (the LPs) for the right to use the olive presses, say $10.

Now, let's look at the two payoff scenarios at the end of the day.

Scenario 1: Price Stays Below $3,100 (A Poor Harvest)

- The Trade: At the end of the fixed duration, the price of ETH did not rise above $3,100. The right to take the ETH at $3,100 is worthless.

- The Analogy: The olive harvest was poor. Thales loses his $10 deposit and dignity as the press owners keep the deposit while laughing at him for believing that olive (ETH) will have increased demand.

- The Settlement & LP Benefit: The trader's option expires. The LP's ETH was never touched. The LP's benefit is clear: they keep the entire fee the trader paid as pure, risk-free yield. They earned extra income on their assets simply for making them available to be borrowed.

Scenario 2: Price Rises Above $3,100 (A Bountiful Harvest)

- The Trade: At the end of the fixed duration, the price of ETH is miraculously $3,200. The trader's right to access ETH at the $3,100 price point is highly profitable.

- The Settlement & LP Benefit: From the LP's perspective, let's say their ETH was placed in a concentrated range between $3,000 and the $3,100 tick. As the price of ETH went past $3,100, their ETH would have been naturally sold for USDC by the AMM's core mechanism anyway. The protocol ensures this happens flawlessly. The trader, now in control of ETH worth $3,200, sells it on the open market (or through the DEX's swap function), uses $3,100 of the proceeds to pay the LP their full due in USDC, and keeps the $100 difference. Thus the trader spent $10 to make $100 ($90 profit). The LP is perfectly compensated, receiving the exact outcome they would have in their concentrated liquidity, plus the initial fee they collected.

The Drawback and the Vault-Based Solution

The primary drawback of this powerful mechanism is that it relies on individual LPs manually placing liquidity in specific, concentrated ranges. This is unrealistic to expect at scale.

This is where the DEX can innovate further by offering sophisticated Structured Vaults, either run by the protocol itself or by sophisticated market-making partners. LPs no longer need to think about ticks or ranges. They can simply deposit a single asset (like ETH) into a vault. The vault's automated strategy then takes on the complex task of placing that liquidity across various future price ticks, effectively turning the LPs' idle assets into an "options-writing" yield product. This makes the entire primitive accessible to passive LPs and ensures there is always a deep supply of "tick liquidity" for traders to borrow from.

New Primitive #2: Shorting New Launch Tokens

One of the biggest inefficiencies in DeFi today is the one-sided nature of new token launches. On platforms designed for rapid, permissionless token creation, markets are often driven purely by buy-side hype with no natural mechanism for sell-side price discovery. A trader who believes a new token is worthless has no way to express that view in the market.

The integrated lending model fundamentally solves this by enabling permissionless shorting for any token launched on the DEX.

How It Works:

This unlocks a simple, powerful mechanism for short selling:

- The Setup: A new token, $SHITCOIN, launches on the DEX. A trader believes it is overvalued and its price will fall.

- Post Collateral: The trader first deposits a trusted asset, like USDC or the native MON token, into their main margin/lending account on the DEX. This collateral acts as a security deposit for the loan.

- The Borrow: The system checks the value of their posted collateral and allows them to borrow $SHITCOIN up to a certain safe loan-to-value (LTV) ratio. The borrowed $SHITCOIN comes directly from the liquidity provided by LPs in the SHITCOIN/MON pool.

- The Short Sale: They immediately sell the borrowed $SHITCOIN on the DEX's spot market, receiving MON in return. At this point, they are "short" the token.

- Closing the Position: To close their short, the trader does the reverse: They buy back the same amount of $SHITCOIN from the spot market (ideally at a much lower price). They repay the $SHITCOIN loan to the liquidity pool, plus any accrued borrowing interest. Once the loan is repaid, their original USDC or MON collateral is fully unlocked and returned to them. The profit is the MON they gained from selling high and buying low, minus the borrowing fees.

The Impact: A Mature Market from Day One

This feature is a game-changer for market health and efficiency.

- Two-Sided Price Discovery: For the first time, a new token launch is met with both buy-side pressure from speculators and sell-side pressure from skeptics. This leads to a much faster and more rational price discovery process.

- A Deterrent to Scams: The mere existence of this feature disincentivizes bad actors. Launching a worthless token on this DEX means it can, and likely will, be immediately shorted to zero, providing a powerful community-driven mechanism for market hygiene.

Of course, this comes with its own risk dynamics.

- LPs providing liquidity for a new token are taking on the risk of their asset being shorted, and the interest rate to borrow these volatile assets would need to be dynamically high to compensate them.

- Shorters can get liquidated on their collateral if the token price pumps upwards against their position.

But the point is that it allows for a fair playing field rather than a one-sided casino. This transforms the DEX into a venue for serious traders and mature assets from the moment of their creation.

How Monad makes this Integrated DEX Viable

This vision of a self-sustaining DEX with integrated lending and advanced derivatives is the the pinnacle of onchain complexity (need to manage swaps, loans, collateral, dynamic interest rates, and complex settlement logic all at once) which may be congested on a sequential chain.

Here're some of the many ways Monad makes it possible:

A Robust Settlement Layer for Complex Primitives: Advanced features like "tick-based borrowing" require complex, multi-step transactions at settlement. Monad's high gas limits and asynchronous execution create the necessary time and computational budget within each block to settle these sophisticated transactions reliably and atomically without failing due to "out of gas" errors, giving developers the confidence to build them.

A Safer, Hybrid Oracle Model: While the DEX can use its own internal TWAP for prices, this creates manipulation risk. A safer model is a hybrid approach. Monad's high transaction frequency makes the internal TWAP more robust and harder to manipulate. Its sub-second block times allow high-frequency updates from external oracles, which can act as a crucial, low-latency "guardrail" to detect anomalies and protect the protocol.

The Precondition for Sophisticated Partners: The success of features like Structured Vaults depends on attracting sophisticated market-making partners to run them. These professional players are extremely sensitive to three things: operational costs (gas), execution risk (latency), and systemic platform risk. Monad is uniquely positioned to satisfy all three requirements.

- Cost & Latency: It provides an environment with ultra-low transaction costs and minimal latency risk (via 1-second finality), making advanced strategies profitable and practical to run on-chain.

- Resilience & Censorship Resistance: Monad's commitment to true decentralization (globally distributed set of over 100 validators that are not co-located) provides a crucial layer of security. For an institutional partner, this is not an ideological preference; it's a fundamental risk assessment. It ensures that their complex, high-value transactions won't be arbitrarily blocked and that the platform isn't vulnerable to a single point of geographic or regulatory failure.

These reasons are exactly why teams like @CapricornDEX, founded by veterans from dYdX and Robinhood, are building exactly these kinds of sophisticated, HFT-grade liquidity solutions designed for professional market makers. The combination of Monad's technical performance and credible neutrality attracts institutional-grade participation.

Conclusion: The Blueprint for a Billion-Dollar DEX

The path to creating a category-defining DEX isn't paved with incremental improvements. It's built on foundational shifts that solve the core, multi-billion-dollar problems of liquidity fragmentation, capital inefficiency, and idle assets.

The three innovations we've explored, the Omnibook, the Parallelized Liquidity Orderbook, and Integrated Lending, are not just features; they are the architectural pillars of a true DeFi powerhouse.

Individually, each is a compelling project. Together, they create a self-reinforcing flywheel:

- The Omnibook pulls in the entire universe of external liquidity, solving for market depth.

- The PLOB engine makes every dollar of native capital hyper-efficient, solving for capital efficiency.

- Integrated Lending turns the entire platform into a yield-generating machine, solving for asset productivity.

Building this unified system is a monumental engineering challenge. It requires more than just a fast blockchain; it demands a platform built on two fundamental principles: Unprecedented Performance and Unshakeable Neutrality.

This is where the Monad thesis of speed without sacrifice becomes clear.

- The Performance: The raw power of async and parallel execution, the efficiency of MonadDb, the 1B gas per block, the 1-second finality are the technical prerequisites. They are what make the high-frequency state updates, the complex atomic settlements, and the real-time risk management computationally and economically feasible.

- True Decentralization: Monad's commitment to decentralization is needed to be the blockchain for all of finance. For the sophisticated partners and institutional capital required to power this vision, this is not an ideological preference; it's a fundamental risk assessment. It guarantees credible neutrality and resilience against single points of geographic or regulatory failure.

This blueprint is not for the faint of heart. It is for builders who want to create not just another DEX, but a foundational piece of DeFi's future infrastructure.

The future of DeFi requires bold ideas. At Monad, we're not just building a faster chain; we're creating a platform for developers to build the impossible.