Prediction Markets Cannot Agree on the Truth

michaellwy

@michael_lwy (opens in new tab)- Published on

- · 8 min read

Have thoughts on this topic? Join the conversation on X.

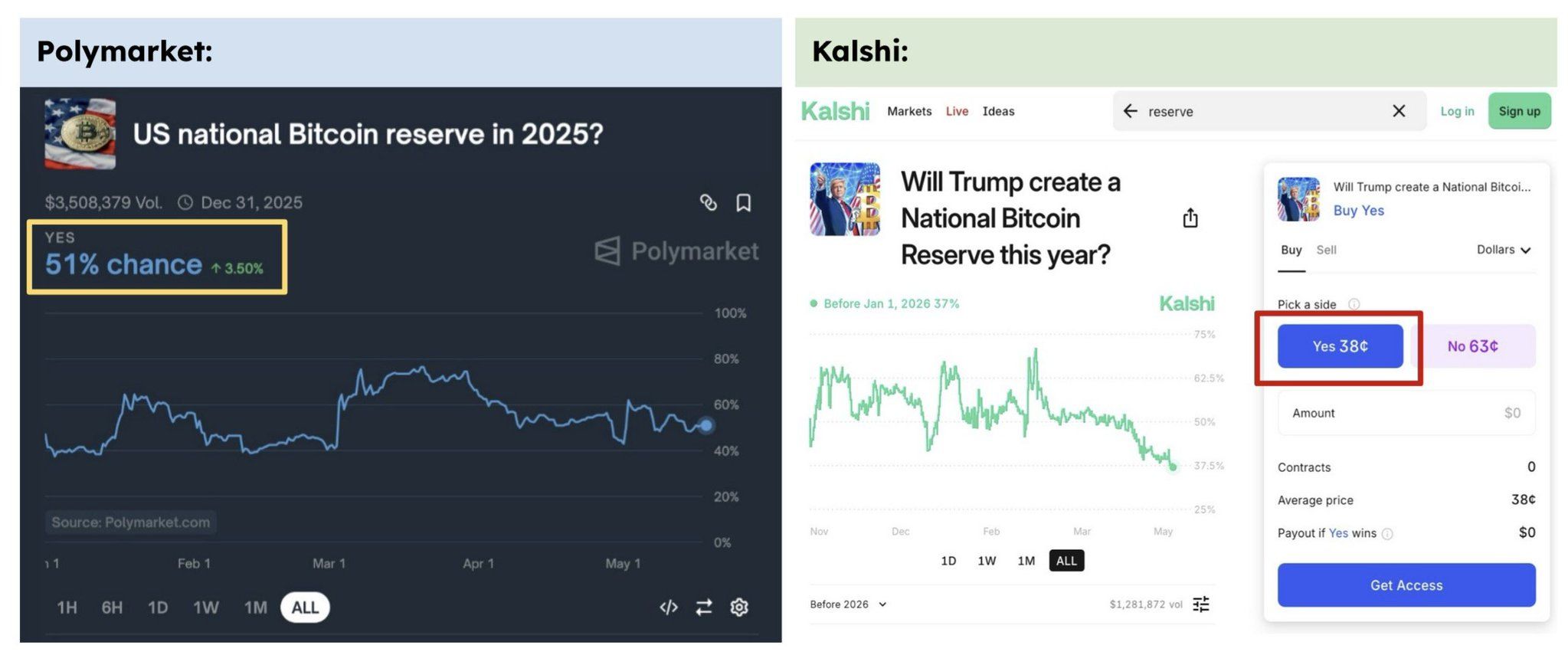

As of the time of writing, the odds of a US National Bitcoin Reserve in 2025 on Polymarket are 51%. Let’s check another prediction market, Kalshi, which has a similar market called "Will Trump create a National Bitcoin Reserve this year (2025)?" Its odds are trading at 37%.

The odds of Yes on Polymarket (51%) + odds of NO on Kalshi (63%) add up to more than 100%, indicating an opportunity for arbitrage. How can I earn guaranteed money? Let’s say I have $10,000. I can simply:

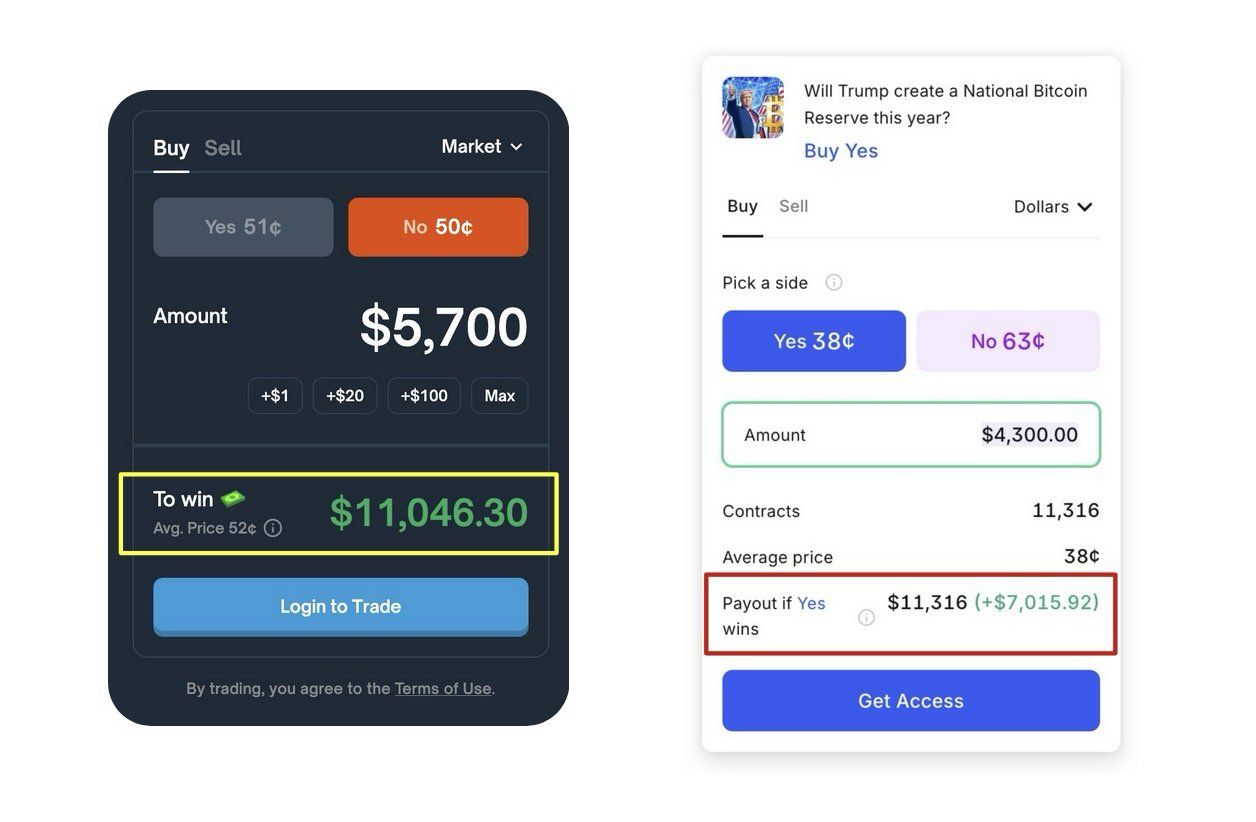

- Spend $4,300 to buy "Yes" on Kalshi,

- And $5,700 to buy "No" on Polymarket.

My expected payout in both markets would be around$11k, which is higher than my principal of $10k. So no matter the outcome of the Bitcoin reserve decision by the end of the year, I net a guaranteed profit! Bam! I’m so smart.

Yet noticing this arbitrage opportunity doesn’t take a genius. In an efficient market, these price discrepancies are usually arbitraged away by sophisticated traders before you even see them

The mirage of free money

So what’s the reason? Why hasn’t this been arbitraged away? The devil is in the details.

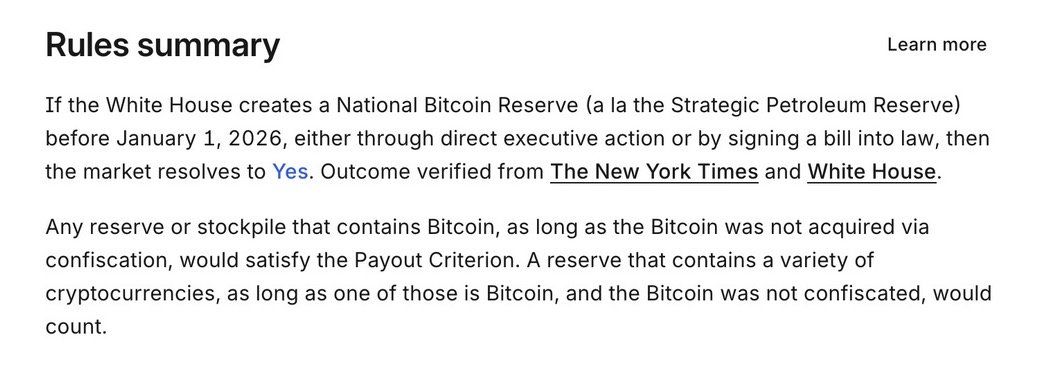

If we take a closer look at each market’s rules, we’ll see that despite the similar headlines, there are subtle differences in what they’re actually predicting. Here are the detailed market rules for each.

Polymarket rules:

Kalshi rules:

A closer look reveals that these rules differ in these aspects:

1. Definition of the asset - Polymarket only needs the government to “hold any amount of bitcoin.” Kalshi needs a designated National Bitcoin Reserve, comparable to the Strategic Petroleum Reserve.

- So if the government buys 10 BTC for the Fed’s balance sheet → Polymarket resolves Yes, Kalshi No.

2. Resolve criteria - Polymarket cites “official info or consensus of credible reporting.” Kalshi will only accept confirmation from the White House or NYT.

- So if a bitcoin reserve is disclosed in a U.S. Treasury FAQ page, Polymarket resolves Yes but not Kalshi until NYT/White House writes it up—or ever.

3. Timing window - Both end 31 Dec 2025, but Kalshi’s rule is “before Jan 1 2026”; Polymarket requires the holding to occur during 2025.

- So if Trump signs a reserve bill on 31 Dec 2025 but the government won’t officially hold any during 2025 → Kalshi Yes, Polymarket would be No.

Now you can see how this arbitrage could fail. The strategy assumes both markets will resolve to the same outcome, allowing you to profit from the price difference. But if they resolve differently, you could lose everything.

In this case, Kalshi's lower probability (37% versus 51%) reflects its stricter conditions. It requires official NYT or White House confirmation rather than just proof of government bitcoin holdings. These additional hurdles make a "Yes" resolution less likely.

The situation of divergent market outcomes is not a conjecture. As I detailed in my previous article about prediction market failures, we've seen this exact scenario play out. During the 2024 US government shutdown debate, Polymarket resolved to "Yes" despite no actual shutdown occurring, while Kalshi correctly resolved to "No."

The oracle is the product

I’m not here to re-hash Polymarket’s sometimes poorly written market rules or UMA’s optimistic-oracle drama. I covered that last time, and Luca Prosperi’s Dirt Road post on Corruption Value Multiple (CVM) does it better than I can.

What interests me is the bigger lesson about prediction markets and how they are different from a typical exchange platform. For any exchange, the main things people look for are:

- what can I buy? (asset listings)

- in what size can I trade? (liquidity/order-book depth)

- how expensive is it to trade? (fee structure)

- how intuitive is the interface? (trading features, good UX)

- is the platform stable and secure? (trustworthiness)

But prediction markets add an extra competitive dimension:

- who is the referee determining the outcome and what rules are they abided by?

In traditional exchanges where fungible assets are traded, there is a strong network effect where larger venues attract more users and liquidity, which in turn attract even more users, leading to winner-take-all or winner-take-most outcomes.

Prediction market contracts are inherently non-fungible. As shown earlier, naive users might see identical headlines, but under the hood they are betting on completely different rule books and referee systems.

Liquidity is not everything for Prediction Markets

The bigger point I’m trying to make is that these resolution quirks don’t just create one-off trading surprises. Instead they shape the competitive landscape of prediction markets themselves. A platform’s choice of rules and oracle becomes its brand, and traders cluster where the referee matches their worldview. The liquidity network effect therefore is only magnetic inside one well-defined rule set, but the second you tweak how “truth” is declared you’ve minted a non-fungible product.

Traders on prediction markets will need to choose carefully the interpreters they trust in addition to things like trading features and tight spreads. This keeps the prediction markets landscape looking more like a patchwork of newspapers (h/t to @llamaonthebrink) than a single NYSE-sized exchange dominating all.

A prediction contract is, on the surface, a yes/no bet on an event. Under the hood, it’s a legal-and-code wrapper that expresses the view that:

- “It will pay $1 if and only if outcome U is judged true by source X, before deadline Y, under appeal path Z.”

Change any of X, Y, or Z, and the nature of the bet changes. That new outcome is a different financial good which is non-fungible in the same way a Reuters story differs from a Fox News article even when both cover the same event.

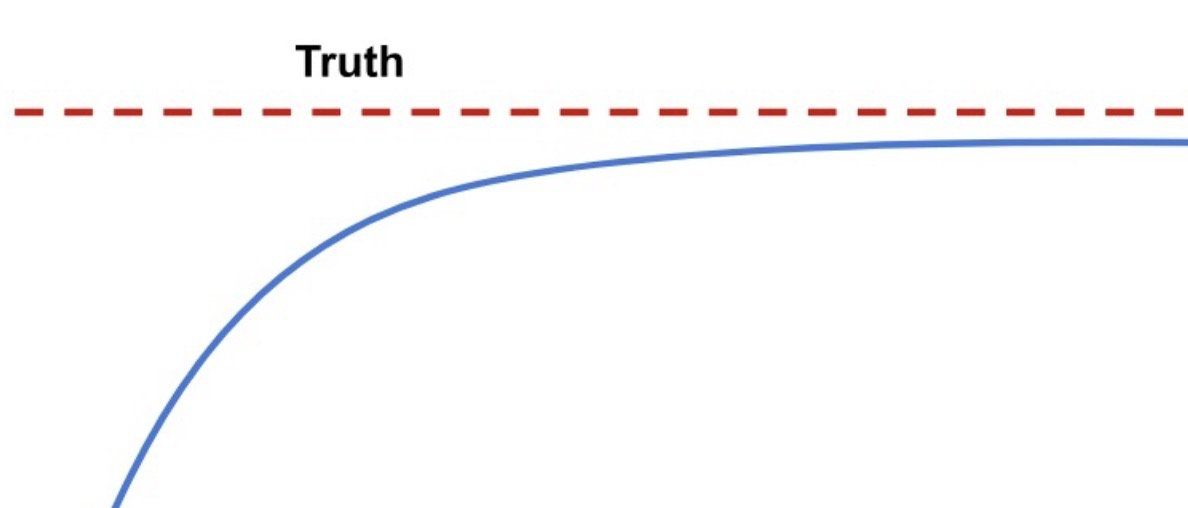

Despite their ambitious goal to “reflect real-world probability,” prediction markets never reach beyond their oracles. What the contract is really pricing is the chance that a particular referee will say it happened. Better oracle design can push the odds closer to “truth,” yet that line is an asymptote—always approached, never touched.

Different communities trust different referees, so likely no single framework can satisfy everyone. The result is permanent fragmentation, much like rival newspapers that coexist precisely because they interpret facts through different lenses.

Back to our Kalshi vs. Polymarket example:

- Polymarket runs on a “we’ll know it when we see it” ethic. A rule might start with “official government statement” but then adds the escape hatch like “a consensus of credible reporting will also be used.” So if a dispute arises, the question falls to a vote of UMA token-holders. In other words, the final referee is a crypto crowd that decides case by case what counts as “credible.”

- Kalshi makes a different editorial choice. Its rule names the White House or The New York Times as the only acceptable sources. That reflects a worldview where those institutions remain the gold standard. Instead of routing disputes to a DAO, they go to Kalshi’s internal team and, if needed, regulators and courts.

The 14-cent price gap we see here is therefore the cost of crossing from one worldview to another. In a future where prediction markets become mainstream, people will likely look to the referees they’re willing to trust besides odds and liquidity.

Conclusion

Prediction markets are tools that turn private insights into publicly priced odds, and then, through their chosen oracles, try to solidify those odds into common knowledge. Since human societies rarely agree on who should define truth, each prediction market ends up forming its own silo, with its own oracle and rules, instead of converging on a single shared system. That’s why I think the prediction market landscape will be fragmented: different referees lead to separate networks, each limited by the boundaries of its own community’s trust.

For prediction market builders, this is both a challenge and an opportunity. These platforms aren’t as interchangeable as typical asset exchanges, because the core difference lies in how they set rules and handle disputes. Better UI or deeper order books are essential edges but likely won’t be enough. Earning user trust requires careful design of the referee system and clearly defined rules. At the same time, that also means today’s incumbents may not be as insurmountable as they seem. Trust can evaporate quickly after a black swan event, opening the door for new entrants.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, legal, or tax advice. Nothing contained in this article should be construed as a recommendation to buy, sell, or hold any financial asset. Always do your own research and consult with a licensed financial advisor before making investment decisions.