The DeFi Mullet Is Growing Up (Or Longer)

Harry Alford

@HarryAlford3 (opens in new tab)- Published on

- · 5 min read

Why the next phase of onchain finance won't look like crypto and why that's exactly the point.

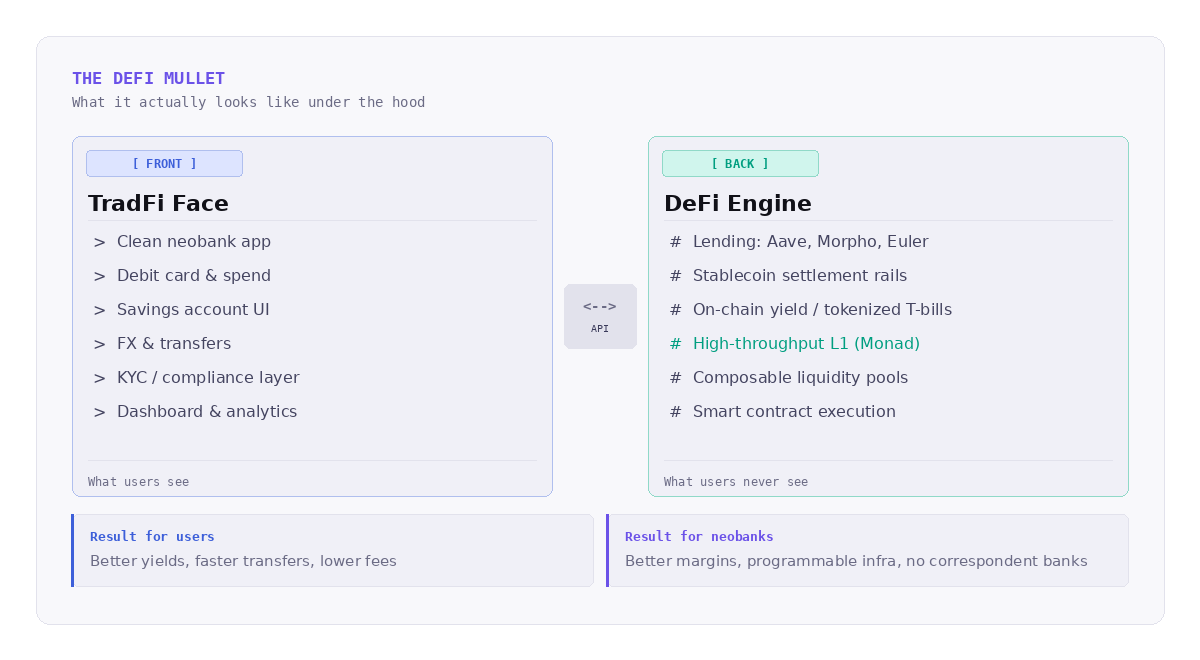

There's a concept that's been floating around DeFi circles for a while now, the "DeFi mullet": TradFi in the front, DeFi in the back. The idea that the best consumer financial products will wear a familiar, friendly face while running on decentralized infrastructure underneath. While it's an intelligent framing, I think we're entering a new phase, and what I'm seeing built on Monad makes me believe the mullet is about to go mainstream.

"Business in the front, DeFi in the back" used to be a fun metaphor. Now it's a product roadmap. The neobanks building on high-performance chains aren't experimenting, they're shipping.

What's Actually Changing

The honest story of DeFi's first decade is that the technology outpaced the experience. The yields were real, the composability was genuinely novel, but the UX was a wall: wallets, gas, slippage warnings, bridge nightmares. For 99% of people who just want a savings account that actually earns something, it was too much friction.

Neobanks changed retail banking by removing friction from the traditional system. They didn't teach people about SWIFT rails or correspondent banking. They just made it fast and clean. The same playbook is now being applied to DeFi, and the infrastructure is finally ready to support it.

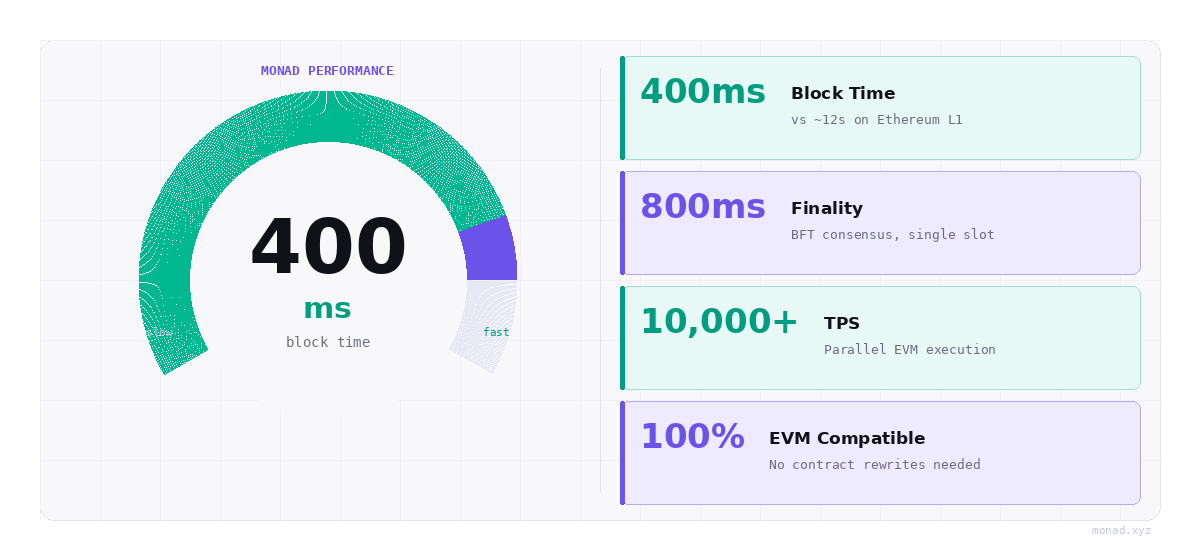

That's what I keep coming back to when I think about what Monad enables. The reason the DeFi mullet stalled wasn't a lack of vision, it was a lack of throughput. You can't build a consumer savings product on infrastructure that confirms transactions in 12 seconds and breaks under load. Users have been trained by Venmo and Robinhood. Their tolerance for latency is zero.

Where This Is Heading

The most exciting neobanks aren't the ones asking "How do we explain DeFi to our users?" They're the ones asking, "How do we make this invisible?" For yield-bearing accounts, instant credit lines, seamless FX, most won't be branded as crypto products despite being powered by onchain liquidity protocols behind the scenes. The most important DeFi products of the next three years will be ones where users never know they're using DeFi at all, or at least don't feel like they're DeFi.

For that to work, two things need to run in parallel: fast, reliable execution infrastructure and battle-tested liquidity protocols.

Protocols like Aave, Compound, and their successors aren't just code, they're trust primitives. When a neobank wants to offer embedded lending, it needs to plug into something with a long security track record, deep liquidity, and known behavior under stress. Building a bespoke lending protocol from scratch is not a risk a consumer fintech should take. However, plugging into a proven protocol is a necessary step.

What's encouraging is that teams building serious lending infrastructure are choosing to build with the Monad ecosystem. Morpho and Euler bring universal lending networks. Gearbox opens up permissionless credit markets. Upshift provides vault infrastructure for tokenized asset management. Neverland and TownSquare are building self-repaying loans and modular money markets on Monad, respectively. The list only continues to grow.

Monad isn't a chain waiting for liquidity protocols to show up. They're already building on the Monad network, drawn by its high-performance execution environment.

The Stack Is Coming Together

What's emerging on Monad is the beginning of a cohesive infrastructure stack for the DeFi mullet era:

- High-throughput, low-latency execution that can handle consumer-scale volume

- Full EVM compatibility, so existing Ethereum ecosystem tooling and integrations work seamlessly

- Battle-tested DeFi primitives (lending, liquidity) available from day one rather than being bootstrapped

- A growing cohort of fintech builders who are explicitly targeting the neobank integration use case

The EVM compatibility piece is underrated from a fintech perspective. Most of the teams building neobank-adjacent products are already in the Ethereum ecosystem. They have smart contract audits, wallet integrations, and tooling. Deploying to a new chain usually means rebuilding or porting everything. Monad's compatibility means businesses can go live on a much faster network with significantly less additional engineering work. The time-to-market advantage is real.

What Comes Next

In the next 12-18 months, we'll see a wave of fintech products launch that, if you read their marketing materials, you wouldn't immediately recognize as DeFi at all. Savings products with competitive yields. Credit products that don't require 150% collateral because they're integrated with real identity and compliance layers. Treasury management tools for small businesses that are accessing onchain liquidity without the treasury team needing to understand AMMs.

The DeFi mullet was always a good idea. The infrastructure to make it real is here now. And Monad is shaping up to be the settlement layer where a meaningful chunk of it gets built.

The opportunity for neobanks and fintechs isn't to become DeFi companies. It's about using DeFi infrastructure the same way they use AWS, as a reliable, scalable backend that users never have to think about.

The mullet is growing up (or longer). And it's starting to look a lot like the future of consumer finance.