The Rise of Local Stablecoins

Harry Alford

@HarryAlford3 (opens in new tab)- Published on

- · 6 min read

Have thoughts on this topic? Join the conversation on X.

- Part I: The Local Stablecoin Moment

- Part II: Brazil, Where Local Stablecoins Go Mainstream

- The Next Chapter

Part I: The Local Stablecoin Moment

Stablecoins proved their initial worth by going global. As digital assets pegged to a stable value, most commonly the US Dollar, they combined the speed and accessibility of blockchains with fiat money. For millions, they became a practical response to friction in the traditional banking system, offering a faster and cheaper alternative to cross-border remittance networks like SWIFT.

While stablecoin’s utility of moving value across borders is clear, a new question emerges: can this technology now build better financial infrastructure within borders?

Source: @jonggal45

The evidence for this shift is most visible in emerging markets, where adoption is driven less by speculation and more by tangible utility. Beyond international transfers, stablecoins are becoming a default financial rail for daily life used for savings, salaries and payments in regions where banking services are unreliable.

This utility is delivered through Web3 neobanks, which are digital-first financial institutions that operate exclusively through mobile apps without physical branches. In places where traditional banks fall short, these platforms are increasingly becoming the preferred way to save and move money.

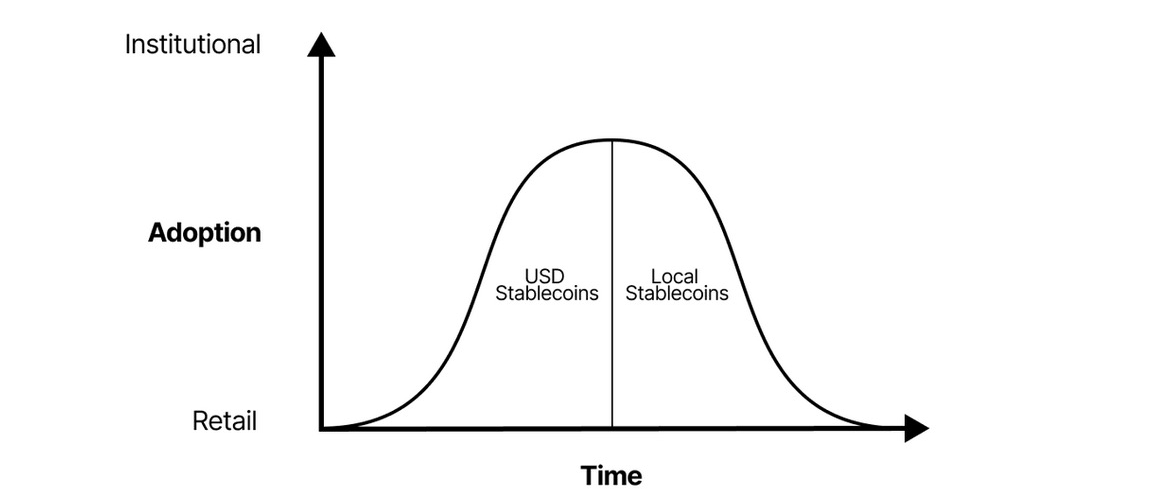

This sets the stage for the phase of adoption: the rise of local stablecoins. In contrast to their global, USD-pagged predecessors, these digital currencies are pegged to domestic units like the Brazilian Real or the Nigerian Naira. They are built specifically to serve local economies, enabling transactions in their day-to-day, bringing the benefits of onchain programmability to the regional level.

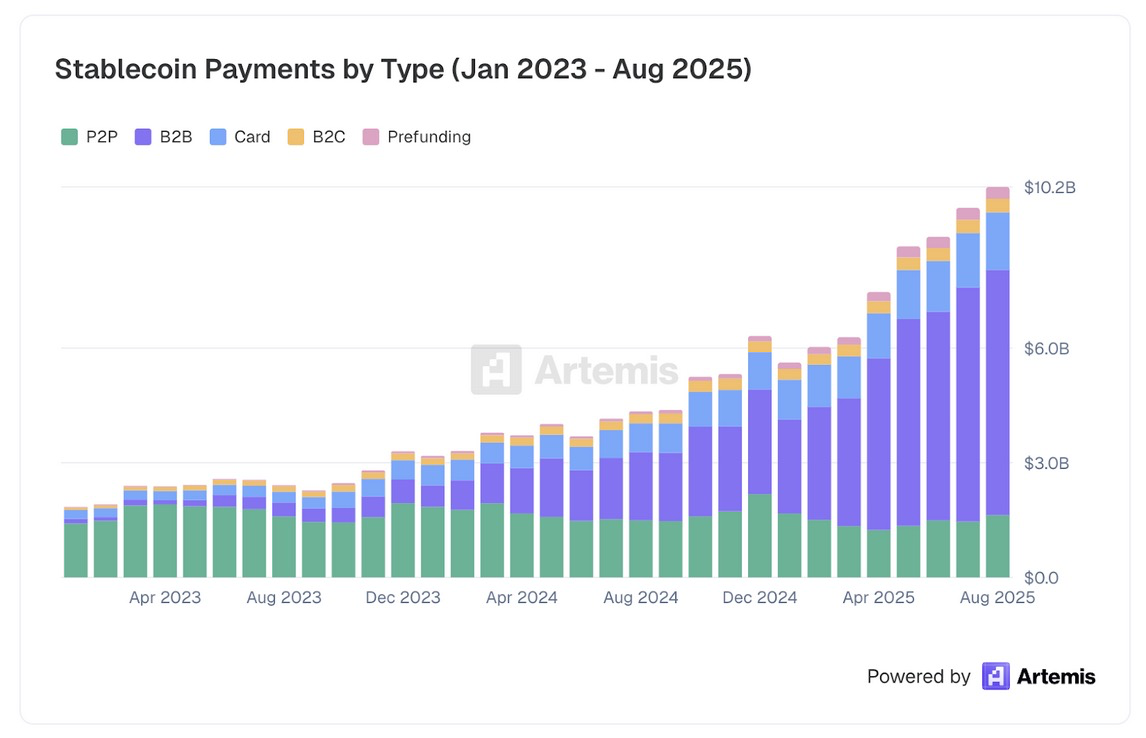

Onchain Economies From the Ground Up

Source: Artemis "Stablecoin Payments From The Ground Up"

The Ethereum Foundation’s Head of Ecosystem recently stated that developing countries account for the majority of onchain activity via mobile wallets. India, Nigeria, Indonesia, and Argentina together represent over 50% of monthly active mobile crypto users, suggesting that these populations use crypto not to speculate but to transact.

That’s the heart of the story: in emerging markets, crypto isn’t speculative infrastructure. It’s financial infrastructure.

The Case for Local Stablecoins

Most stablecoin flows today still follow the de facto pattern: fiat → USD stablecoin → fiat. Each hop adds hidden fees and inefficiencies: two currency conversions (into and out of USD) plus the overhead of moving through intermediaries like on/off-ramps. It’s a system optimized for global flows, not local realities, one that endures more from legacy than logic.

Whether you’re sending pesos, reales, or whatever currency, the recipe stays the same: everything gets funneled through dollars,” says Frontera. “That’s fine if you need USD on the other end. But if what you’re after is local cash, the route stops making sense. A better model is unfolding: fiat → local stablecoin → local stablecoin → fiat. A leaner, local-first design that finally speaks the language of emerging economies.

And as stated in the Dune LATAM Crypto Report:

By removing the need for constant USD-fiat conversion, they (local stablecoins) cut costs for merchants and users while speeding up settlement for local commerce.

Local stablecoins such as BRL (Brazil), NGN (Nigeria), IDR (Indonesia), SGD (Singapore), and PHP (Philippines) are emerging as the connective tissue between Web3 infrastructure and real economies. They maintain the stability and programmability of digital money while grounding it in the familiarity of local currency.

Part II: Brazil, Where Local Stablecoins Go Mainstream

If local stablecoins represent the next chapter of financial infrastructure, Brazil might be the first country writing it in real time.

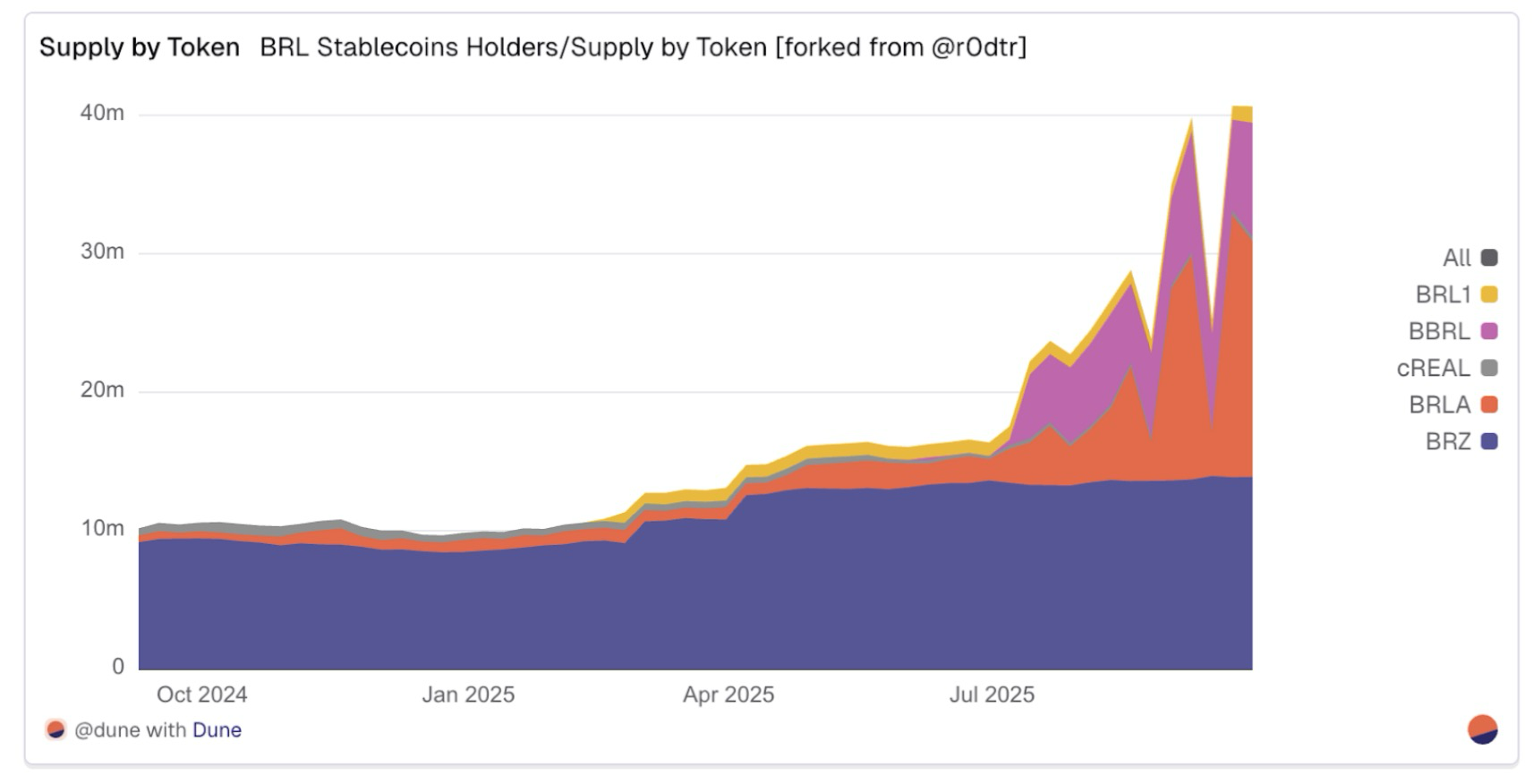

Latin America’s $1.5 Trillion Crypto Economy

According to Chainalysis, LATAM saw over $1.5T in crypto inflows last year, including $319B in Brazil alone, where nearly 90% of volume came from stablecoins, not speculative tokens. Key players like Mercado Bitcoin and the launch of the BRL1 stablecoin have fueled this growth.

Source: Dune LATAM Crypto 2025 Report

At least five stablecoins pegged to the Brazilian Real (BRL) are gaining traction. In markets like Brazil, local stablecoins are already money. They power everyday transactions, from paying rent to buying coffee: no exchanges, no speculation, just seamless, usable value.

The Roadblocks To Real Adoption

Despite year-over-year growth, local stablecoins still face structural challenges. For one, USD-pegged stablecoins are still the popular choice to preserve wealth and use as a hedge against inflation. The total stablecoin market cap is over $300B, with a majority pegged to USD, like USDC and USDT. The largest non-USD stablecoin, EURC, has a market cap of only $283M. Additionally, liquidity, regulatory uncertainty, high conversion costs for users and merchants, and fragmented infrastructure remain barriers. At the same time, each barrier represents an opportunity for builders.

For example, Picnic is a Brazilian-based non-custodial neobank that links cards to stablecoin wallets, allowing users to transact in local stablecoins and spend directly from their onchain balance without off-ramping. Picnic also solves major pain points for non-crypto native users by offering unique on/off-ramps for local stablecoins with zero-fee and tax advantaged conversions through direct integration with Brazil’s instant payment ecosystem, PIX. The result is fast, affordable global access, seamless currency conversion, built-in yield, and crypto purchase options.

Brazil is not only a great template for how local stablecoins, driven by strong builders and issuers, lower the barrier to entry for new users and reduce or eliminate ramping costs. It may also be the ideal proving ground for real stablecoin adoption. As Iporanga Ventures notes:

As the market evolves, it has the potential to absorb a significant share of operations currently conducted on traditional rails. Last year, BRL stablecoins transacted over US$920 million. Looking ahead, for example, in the Trade Finance and Remittance sectors, even if they capture just 10% of the existing market, BRL stablecoins could facilitate transactions exceeding US$132 billion annually. This shift could generate savings of up to US$6.6 billion by reducing transaction and intermediary costs. When considering additional market segments, such as credit, the overall cross-border payment market, and inter-protocol settlements, the impact could be even greater.

The Next Chapter

From São Paulo to Lagos to Manila, a new financial stack is taking shape. One that’s local-first, stablecoin-native, and built around mobile experiences wrapped in neobanks.

USD stablecoins were just the beginning. If onchain finance is going to serve the real economy, it has to speak more than one language. The next chapter will bring shillings, rupees, yen and more.