Everything You Need to Know About Tokenized Equities

fishmarketacad

@FishMarketAcad (opens in new tab)- Published on

- · 23 min read

Have thoughts on this topic? Join the conversation on X.

The first time I touched tokenized stocks seriously was when Robinhood removed the buy order on GME stock, and I saw people talking about @mirror_protocol (even CZ chimed in) as a fully permissionless onchain alternative for trading stocks and I was intrigued and checked it out.

I still remember being early and the APY was over >100% for providing liquidity on mAsset-UST pairs. I tried it out and was hooked by the ease of use, vision, and yield, and even wrote an article on it. So it's pretty ironic that the reason why tokenized stocks came into the spotlight again was because of Robinhood's announcement of launching tokenized US stocks for European customers and even their own L2 chain.

I'm still seeing some confusion over tokenized equities, so thought I would share my thoughts about it. In this article I explore:

- 1. What Are Tokenized Equities and How Do They Work Legally?

- 2. Why Tokenized Equities? Bull and Bear Case

- 3. Spot vs. Perp Equities: Utility and Hurdles

- 4. The Future of Tokenized Equities

1. What Are Tokenized Equities and How Do They Work Legally?

Before jumping into the pros and cons of spot vs perp tokenized equities and their use cases, let's explore why they weren't popular previously and why they are getting some traction now.

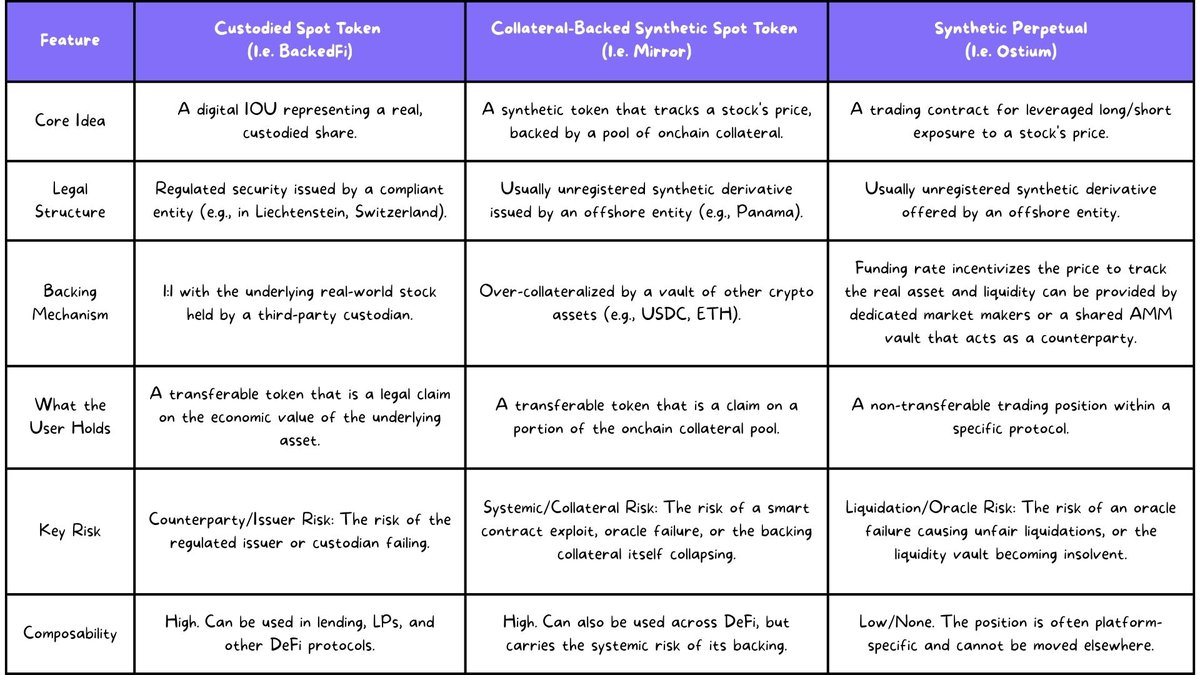

tldr; here's a comparison table of the different approaches.

Feel free to skip the rest of this section if it doesn't interest you.

Regulatory and Legal Maze

Although creating tokenized equities is a technical challenge, the legal challenge is much more tricky.

For years there was a lack of clear rules in major jurisdictions like the US which has pushed crypto companies to crypto-friendly environments with legal clarity like Liechtenstein. Thanks to their progressive "Blockchain Act." which is legislation that provides a clear legal framework for issuing tokenized securities.

It introduced the legal concept of a book-entry system (Wertrecht), which allows securities to be "dematerialized", meaning the functions of a physical stock certificate can be legally replaced by a digital entry.

This provided the legal certainty needed to represent real-world assets as tokens on a blockchain.

How Backedfi is doing it

This is why @backedfi chose to operate at Liechtenstein, as they can issue "bTokens," which are ERC-20 tokens representing units of a fully collateralized tracker certificate. For every bCOIN token on the blockchain, there is a real share of Coinbase stock held with a custodian.

This structure separates the regulated issuance process from the secondary market for permissionless trading.

To mint or redeem tokens directly with Backed, users must still be qualified professional investors who pass full KYC/AML checks. And once these tokens exist, they are freely transferable and can be traded by anyone on decentralized exchanges (DEXs) or a select few regulated exchanges.

For qualified investors who are fully KYCed and AML-compliant, redemption of bTokens settles in cash value, not in the underlying shares, as Backed's broker sells the underlying security on the open market and transfers proceeds to the investor, minus a small redemption fee, which is then settled to the investor’s account in fiat or a stablecoin like USDC.

The redeemed bTokens are then immediately burned to ensure the 1:1 backing. This structure is designed to provide the economic benefits of the stock while abstracting away the immense logistical and regulatory complexity of transferring registered securities across international borders.

However bTokens do not have ownership or voting rights. So what rights do they have?

As bToken only represents legal ownership of a tracker certificate, which is a structured product issued by Backed Assets (JE) Limited, a regulated entity in Jersey (USA). The certificate only gives a holder a contractual claim to the economic value of the underlying stock.

Think of it this way: you don't own the house, but you own a legally binding contract that guarantees you will receive the full financial value of the house if it is sold. The bToken is your proof of ownership of that contract. So, your primary right is a financial one: a claim on the value of the asset, not the asset itself.

So what happens to your bTokens if Backedfi disappears overnight?

The underlying shares that back your bTokens are held by a separate, third-party custodian and are legally ring-fenced from backedfi's own assets. They cannot be used to pay the company's debts, aka asset segregation.

So as a bToken holder, you would be a creditor of the issuer, and there would be a liquidation process with the legal issuer which is Backed Assets (JE) Limited, and the proceeds of the liquidation would be distributed to the holders of the tracker certificates (the bToken holders).

So, there is a legal path for value recovery but it's not a simple over-the-counter redemption in Liechtenstein.

tldr; the bAssets likely won't go to $0 but the risk becomes the length and complexity of the liquidation process to claim back the economic value. Actual recovery in a wind-down scenario may depend on legal, operational, and jurisdictional factors outside the user's control.

Who Can Trade These Tokenized Equities?

Depends on which law they operate under. For Backed Assets, it is regulated under European law (specifically in Liechtenstein and Jersey) and is not registered with the US SEC.

The core of the DeFi regulatory challenge is that while the issuer has clear compliance obligations, access control on the secondary market may shift to the various interfaces that allow users to interact with the blockchain. For US persons, bypassing these restrictions to trade these tokens remains a high-risk and non-compliant activity.

How Robinhood is doing it

Robinhood's entry into tokenized equities takes a distinctly different path, one that uses blockchain as a back-end rail while keeping the UX firmly within its centralized, user-friendly ecosystem.

For European customers, Robinhood Stock Tokens are not direct claims on shares but are legally structured as derivatives under MiFID II regulations. When a user "buys" a stock token, they are actually entering into a contract with Robinhood Europe that is designed to track the price of the underlying US stock.

While the underlying assets are held by a US-licensed institution, the tokens themselves are essentially IOUs recorded on a blockchain (initially Arbitrum), with plans to migrate to their own proprietary Layer 2.

This structure gives Robinhood complete control over the user experience and the assets themselves. Key features of their model include:

- A Closed Ecosystem: Currently, users can buy, sell, and hold these stock tokens within the Robinhood app, but they cannot withdraw them to an external wallet or another platform. This prevents the tokens from being used in the broader DeFi ecosystem for things like lending or liquidity provision, fundamentally limiting their composability.

- 24/5 Trading: Robinhood offers around-the-clock trading from Monday to Friday, bridging the gap between European and US market hours. This allows users to react to news and market movements outside of traditional trading windows.

- Seamless Operations: Robinhood handles all corporate actions automatically. For events like stock splits or mergers, they adjust the user's token holdings. For cash dividends, they are automatically paid out to the user in Euros, with no FX fees applied. This focus on abstracting away complexity is a core part of their strategy to appeal to a mass-market retail audience.

In essence, Robinhood is using blockchain as a highly efficient internal ledger to offer derivative exposure to US stocks. It’s a pragmatic approach that prioritizes ease of use and regulatory compliance within their own platform over the open, permissionless ethos of DeFi.

While this closed-system provides a safe, curated experience for their massive retail user base, it fundamentally sacrifices the core promise of DeFi: composability.

By preventing users from withdrawing their tokens, Robinhood effectively blocks them from being used as collateral, liquidity, or building blocks in the broader on-chain economy, leaving a significant opportunity for other platforms to compete not just for users, but to build the truly permissionless and interoperable tokenized assets that will form the foundation of the open DeFi ecosystem.

Regulatory Summary

This global patchwork of regulations has led to two dominant models for bringing equities on-chain:

1. Spot Tokenized Equity (The Digital IOU)

This is the model being pursued by both regulated fintech giants like Robinhood and crypto-native issuers like Backed.fi. The core principle is that for every token on the blockchain, there is a corresponding, real share of the stock held in custody by a regulated financial institution.

- How it Works: The approach varies based on the issuer. A crypto-native firm like Backed.fi buys a real share of a stock (e.g., TSLA), holds it with a custodian, and then mints a corresponding token (e.g., bTSLA) on a public blockchain. This token is a freely transferable, composable asset that can be traded on DEXs, but only qualified investors who pass KYC can mint or redeem it directly. In contrast, Robinhood offers its European customers stock tokens that are legally structured as derivatives under MiFID II. While the underlying assets are held by a US-licensed institution, the tokens themselves are essentially IOUs recorded on a blockchain. This allows Robinhood to offer the economic benefits of the stock in a controlled, centralized environment, where the tokens currently cannot be withdrawn to external wallets. Both methods rely on a regulated entity to custody the underlying asset, but they differ significantly in their approach to open-market composability.

2. Perpetual Futures (The Synthetic Bet) This model doesn't involve direct ownership of the underlying asset at all. It operates in a legally gray area, and platforms must navigate a complex regulatory environment to offer these products.

Examples include @ostiumlabs, @drakeexchange (soon), and even @aevoxyz just launched it with 1000x leverage.

- How it Works: A perp DEX can face significant legal risk for listing equities as perps. Regulators in major markets like the US and EU view a derivative whose value is based on a security (like a stock) as a regulated product itself. Offering these requires specific, and difficult to obtain, licenses. To mitigate this risk, perp DEXes typically employ a strategy of offshore incorporation, establishing their legal entities in crypto-friendly jurisdictions. They combine this with robust geo-blocking on their websites and explicit prohibitions in their Terms of Service to prevent access from restricted countries like the US. While not a foolproof defense, this demonstrates that the platform is not actively soliciting customers from these heavily regulated markets, allowing them to operate in this legally complex space for the time being.

Each of these models offer a unique set of trade-offs, catering to different user needs and risk appetites

2. Why Tokenized Equities? Bull and Bear Case

Most of my friends use IBKR or one of the many brokerages available to trade stocks, so why do we even need tokenized equities? The answer depends entirely on a user’s goals and where in the world the user is located.

Bull Case: More Accessible Global Markets

The strongest argument for tokenized equities lies in their potential to democratize financial access on a global scale.

- Global Financial Inclusion: In the US and Europe, stock market participation is relatively high. But outside of those jurisdictions, only about 5-15% of the population is invested in US stocks. This isn't necessarily due to a lack of interest, but a lack of accessibility doesn't help. Crypto allows people in Southeast Asia or Latin America to get permissionless exposure to US equities with just their phone and internet, bypassing traditional banking requirements.

- 24/7 Market Access for a Global Audience: The US trading window can be inconvenient for those outside the US time zone. For traders in Asia, the market opens in the middle of their night. Tokenized equities break this constraint, offering a 24/7 market that allows anyone, anywhere to trade on their own schedule and react to news as it happens, instead of allowing the privileged few to act on after-market trading hours.

- Permissionless Innovation: Tokenized equities are not just products; they are open financial primitives. Any developer in the world can build a new application on top of them. This could be a hyper-localized, self-custody brokerage app for a specific country, a complex structured product, or an automated yield vault. This unlocks a level of innovation that is impossible in the current siloed ecosystems of brokerages.

- Streamlining Corporate Actions: Corporate actions like stock splits, dividends, and mergers are announced in unstructured formats, this data is then manually re-validated by dozens of intermediaries, a costly process that can cause trade errors. A recent initiative led by Chainlink, in collaboration with giants like UBS, Swift, and Franklin Templeton, is using AI and oracles to eliminate this operational headache. They are building a system to autonomously extract this data, reach a consensus, and publish it on-chain as a "unified golden record." This creates a source of truth that can be consumed programmatically by everyone, from protocols, custodians to asset managers.

Bear Case: Niche Product for a Developed World

However, it's crucial to be pragmatic. For the average investor in a developed country, there is no immediate need for tokenized equities.

- Is It Solving a Real Problem? For a user in the US or Europe, platforms like Robinhood or Interactive Brokers are already extremely cheap, fast to onboard, and easy to use. While the DeFi ideal of self-custody is powerful, the reality is that the user experience of setting up a wallet, onramping, managing gas fees, DeFi navigation, and risking exploits or being drained, does not seem worth it for the mass market.

- Liquidity Fragmentation: The on-chain trading experience is currently inferior for any significant size. Until on-chain markets can offer liquidity and execution quality that is at least comparable to traditional venues, there is little incentive for serious capital to migrate over. This creates a classic chicken-and-egg problem: without deep liquidity, big traders won't come, and without big traders, it's hard to build deep liquidity.

The reality is that the need for tokenized equities is most acute for those who are currently excluded from the traditional system. For the developed world, its true utility will only be unlocked as the DeFi ecosystem matures and the benefits of composability.

3. Spot vs. Perp Equities: Utility and Hurdles

Now that we understand the different legal and technical structures behind on-chain equities, we can explore the practical trade-offs for users. The market has largely converged on two dominant models: the asset-backed spot token, which aims to replicate direct ownership, and the synthetic perpetual future, which is built for capital-efficient trading. While a third model—the collateral-backed spot token (like Mirror Protocol)—exists in theory, it has failed to gain significant traction due to the immense systemic risks associated with its backing mechanism. Therefore, this analysis will focus on the two approaches that are currently defining the future of the space: asset-backed spot and perpetuals.

3a. Spot Equities: Utility & Hurdles

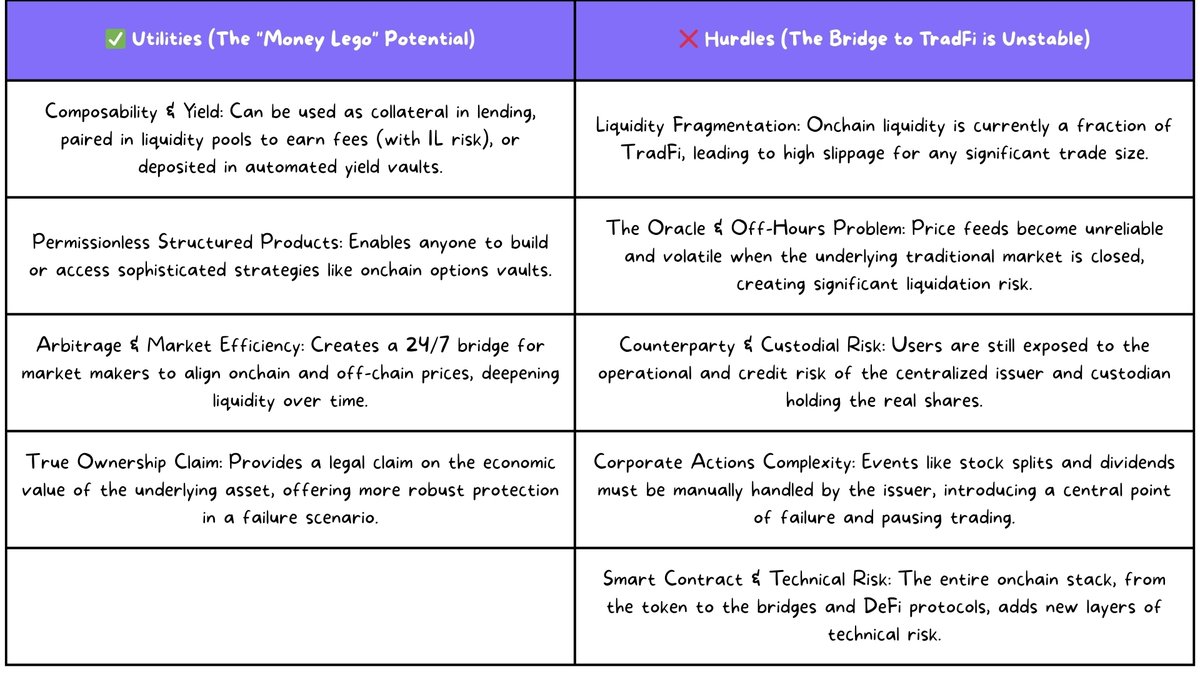

The Utilities

Right now, using a brokerage like Interactive Brokers, you can use your stock portfolio as collateral for a margin loan to trade other assets within their system. But that's where the utility ends. Your assets are siloed.

So I think the real advantage is composability. Right now most of my stocks are just sitting idle in my brokerage doing nothing. By tokenizing them, they can be transformed from a static asset into a dynamic, programmable "money lego", allowing me to be more degenerate capital efficient.

When an equity becomes a token on a public blockchain, it unlocks use cases that are simply impossible in the traditional world:

- Autonomous Yield Generation: A user could deposit their tokenized equity into a yield vault. The vault would then deposit it into a lending protocol that supports it, to earn a base interest rate (realistically near 0%), but more importantly borrow stablecoins against it. It then uses those stablecoins to yield farm elsewhere and then automatically compounding the returns back into the tokenized equity. This turns a passive stock holding into a dynamic, yield-generating asset.

- Permissionless Structured Products: On-chain protocols can democratize complex trading strategies. Once tokenized equities mature, I’m sure there'll be options protocol on tokenized equities as well, and you can imagine a vault that allows anyone to execute options strategy by depositing tokenized stocks. This opens up more yield opportunities that are independent of the crypto market.

- Liquidity Provision: Self-explanatory, basically users can provide liquidity by pairing the tokenized assets with other assets (even other tokenized equities) in an LP and earn a percentage of the trading fees from every swap that occurs in that pool. However they will still be exposed to impermanent loss.

- Fueling Arbitrage and Market Efficiency: Tokenized equities create a direct, 24/7 bridge between on-chain and traditional markets opening up arbitrage opportunities for market makers who have the "plumbing" to connect both worlds. If the on-chain price of tokenized Apple deviates sufficiently from its price on NASDAQ, these arbitragers can buy the cheaper asset and sell the more expensive one, capturing a risk-free profit and peg the prices back into alignment. This can become another yield product that also helps to deepen liquidity and ensure the on-chain market becomes increasingly efficient.

The Hurdles

Despite the immense potential, the path forward is filled with significant complications that cannot be ignored.

- Liquidity Fragmentation: This is the most critical and immediate problem, tokenized equities have nowhere close to sufficient liquidity for any serious volume. In traditional markets, orders can be placed worth millions of dollars on a tokenized asset without significant slippage, but right now even a less than $100k trade results in over a 1% slippage. This is because the vast majority of capital and market-making activity still resides in TradFi. Until that changes, the on-chain trading experience for large volumes of spot tokenized equity will remain inferior.

- The Oracle & Off-Hours Problem: DeFi relies on oracles to know the price of an asset. But when traditional markets close, what is the true price of the asset? If the on-chain token market becomes the only live price feed, and as we saw with the Pax Gold (PAXG) token during a period of geopolitical turmoil, it can be volatile, as PAXG pumped over 20% on low volume. And any oracle reporting that temporary spike as the "real" price could trigger a cascade of unfair liquidations across lending markets and perp dexes, creating a significant systemic risk for anyone using these assets outside of traditional market hours.

- Smart Contract & Technical Risk: Every layer of technology, from the token contract itself to the cross-chain bridge used to move it and the DeFi protocol it's deposited into, introduces a new potential point of failure. Each step in the composability chain adds a new attack surface that may not exist in the traditional, centralized world. Even an established protocol like GMX v1 can get exploited after years of clean track record. I just hope whichever is the leading tokenized stock issuer has very strong opsec and can freeze exploited funds quickly until security becomes more established.

- Counterparty & Custodial Risk: Even with fully-backed spot tokens, users are still trusting a centralized issuer (like Backedfi or Robinhood) and their chosen custodian to properly manage and secure the underlying shares. While these entities are regulated, they are not completely risk-free, and their failure would require potentially lengthy legal process for holders to recover the value of their assets.

- Corporate Actions: Tokenized spot equities must also deal with events like stock splits, dividend payments, mergers, or ticker changes which cannot happen autonomously on-chain. This introduces both a significant technical hurdle and a central point of failure, temporarily breaking the "always-on" promise of DeFi and reminding users of the token's reliance on a trusted offchain operator.

3b. Perp Equities: Utility & Hurdles

While spot tokens aim to replicate asset ownership, perpetual futures (perps) are built for one thing: pure, capital-efficient price exposure. This model is the instrument of choice for active traders, offering a set of tools and advantages that are fundamentally different from holding a spot asset.

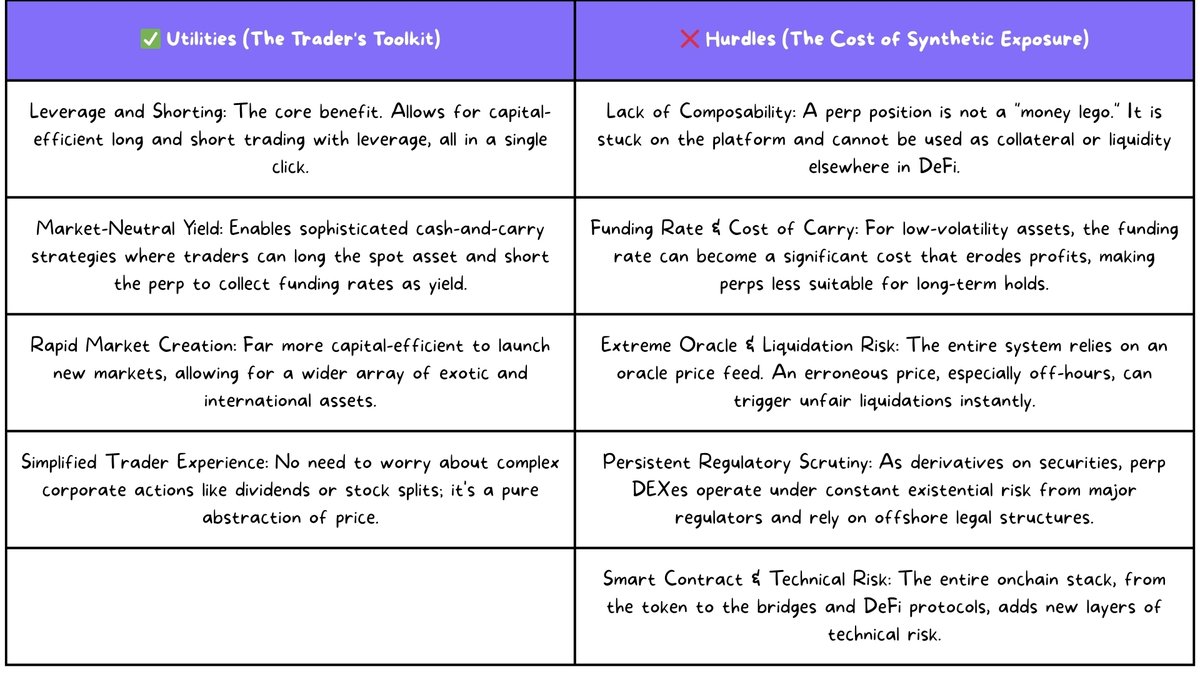

The Utilities

Perp DEXes are not trying to create a new form of ownership; they are building a more accessible and powerful venue for speculation. The benefits are geared specifically towards traders:

- Advanced Trading Capabilities (Leverage and Shorting): The core benefit is allowing traders to go leverage long or short in just a single click, to make it easy to express any market view, bullish or bearish.

- Capital Efficiency and Rapid Market Creation: Launching a perp market is far more capital-efficient than launching a spot token. Instead of needing to acquire and custody millions of dollars worth of the underlying stock, a perp DEX only needs an amm vault with decent TVL with a concentrated liquidity to facilitate trades. This lower barrier to entry allows perp DEXes to be more nimble, potentially listing a wider array of assets that would be challenging to offer attractively via spot.

- Simplified Trader Experience: Because there is no underlying asset, traders do not need to worry about the operational complexities of corporate actions. Dividends, stock splits, and mergers are irrelevant from a mechanical perspective. The instrument is a pure abstraction of price, allowing traders to focus solely on market movements without the administrative overhead of traditional stock ownership.

- Delta-Neutral Yield Vaults: The coexistence of both a spot token and a perp for the same asset can unlock the possibility of market-neutral yield strategies. The most common of these would be the "cash and carry" or basis trade, basically what Ethena does. For example, when the funding rate is positive, a trader can buy the spot tokenized equity (or just the IRL underlying asset) and use it as collateral to borrow USDC to short the perp market, creating a highly capital-efficient yield strategy.

The Hurdles

The advantages of perps come with a significant and distinct set of risks and limitations that users must understand.

- The Lack of Ownership and Composability: A perpetual position is typically not a "money lego," as you cannot withdraw it, lend it, use it as collateral in another DeFi protocol, or provide it as liquidity on a DEX. It is a non-transferable, platform-specific contract, sacrificing the entire world of DeFi composability for trading efficiency. That said if the perp DEX operates its own money market that's vertically integrated (similar to mango markets), it would create more composability within the platform.

- Funding Rate Complexity and "Cost of Carry": Perps rely on a funding rate to stay pegged to the spot price. When market sentiment is heavily skewed, for instance, if everyone is bullish on NVIDIA, longs will pay a continuous fee to shorts. For low-volatility assets like equities, this funding rate can become a major "cost of carry," potentially eroding profits or even exceeding the daily price movement of the stock. This makes perps better suited for short to mid term trading rather than long-term, passive holding, unless you're running a delta-neutral strategy.

- Extreme Oracle and Liquidation Risk: The entire system's integrity rests on the quality of its oracle price feed. A perp's price is only as good as the data it receives. Especially during off-hours when the underlying market is closed, an oracle might pull a temporary, volatile price from an illiquid source. A sudden, erroneous price "wick" reported by the oracle can trigger a cascade of unfair liquidations, wiping out a trader's entire collateral in an instant.

- Persistent Regulatory Scrutiny: As derivatives on securities, platforms offering these products typically operate from offshore jurisdictions and use geo-blocking and other access controls to avoid operating in major markets where activities may be restricted or prohibited like the US. However, this is a reactive defense, and the entire model operates under the persistent, existential risk of a coordinated regulatory crackdown.

4. The Future of Tokenized Equities

Robinhood's entry has transformed the tokenized equity space from a niche experiment into a mainstream race. The coming year will not be about reaching a final destination, but about the crucial, foundational work of building out the infrastructure and liquidity needed for tokenized spot equities to thrive.

Here are the key battlegrounds and trends to watch over the next 12 months.

1. The Great Liquidity Race. The primary challenge for any on-chain tokenized stock market is attracting deep, reliable liquidity. Fortunately, Robinhood, who has deep liquidity and distribution, have their tokenized equity siloed within their own ecosystem, so other tokenized stock issuers have a chance to compete, at least until Robinhood decides to open up their tokenized stocks. I expect a wave of incentive programs, from yield farming rewards to points systems and airdrops, as platforms aggressively compete to attract liquidity providers, traders, and sophisticated market makers. The projects that can successfully solve this "chicken and egg" problem of attracting both flow and liquidity will be the early winners.

2. Paving the Regulatory Pathways. While comprehensive, global regulation is still years away, I believe we will see more issuers follow the model pioneered by companies in Liechtenstein, using its clear legal framework to bring fully-backed spot tokens to market. Similarly, guidance from jurisdictions like Hong Kong will provide a template for other regions to follow. We can also expect the first few cautiously optimistic partnerships between TradFi institutions and regulated crypto firms, as the legacy world seeks a compliant way to engage with this new technology.

3. Composability in Action: The First Real "Money Legos". This is where the true potential of DeFi will begin to shine. With a growing supply of liquid, asset-backed tokenized equities, the next year will see the first real wave of composability. Expect to see governance proposals on major lending protocols to accept "blue-chip" tokenized stocks as a new form of collateral. We will also see the emergence of more sophisticated automated yield vaults that can put these assets to work. Most excitingly, the coexistence of both spot and perpetual markets for the same asset will give rise to the first on-chain automated basis trading vaults, allowing users to deposit capital and earn a market-neutral yield from funding rates to further diversify on-chain yields.

4. The Maturation of the Perp Market. I foresee a bigger focus on listing beyond just the major tech stocks, including HKSE equities and commodities. We will also see significant developments in the underlying technology, with a heavy emphasis on more robust oracle solutions and more sophisticated risk management systems for the liquidity pool that back these perp markets.

If the vision of crypto is to bring everything on-chain, stocks definitely make sense to be on-chain, and it'll be exciting to see how it plays out.

Disclaimer: The views expressed in this post are the personal views of the author as of the time of writing and are subject to change. This content is provided for informational purposes only and should not be relied upon as legal, business, investment, tax or other advice. Neither the author nor the Monad Foundation recommends that any cryptocurrency should be bought, sold, or held by you or that any particular investment strategy should be pursued. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment or investment strategy.