What if AMMs Could Lend?

michaellwy

@michael_lwy (opens in new tab)- Published on

- · 10 min read

Have thoughts on this topic? Join the conversation on X.

Introduction

The basic building blocks of today’s DeFi rest on two primitives: AMMs and lending markets.

On one side are spot liquidity pools like Uniswap. They’re built to facilitate swaps: you put assets in, traders swap against them, and you earn a slice of the trading fees. Most of the time that liquidity is just sitting there waiting. In slow markets, the fees it collects might not even offset impermanent loss.

On the other side are money markets like Aave. These are platforms where you go to lend or borrow. They run on external price oracles and are maintained by governance, which means every new token needs to be reviewed and whitelisted, with risk parameters set by committee. And when a loan becomes too risky, liquidators rush in and close the position before bad debt can occur.

For you as a user, these are two separate worlds:

- The AMM, where you trade.

- The money market, where you lend and borrow.

They don’t share liquidity with each other and they don’t share listings. The separation leaves assets underused, forces multi-step flows, and adds friction to users trying to create leverage positions.

AMM and lending, all in one

Likwid is a DeFi protocol on Monad that combines a decentralized exchange (AMM) with a lending platform. It enables permissionless margin trading without price oracles or direct counterparties.

In simpler terms, users can provide liquidity, earn fees and interest, borrow assets, and open leveraged long or short positions all within one unified system.

In this article, we will take a look at the limitations of today’s DeFi infrastructure and how Likwid’s novel AMM design aims to address them.

How to long/short currently

Let’s walk through how you’d short a token today using AMMs and lending markets the way they’re set up now.

Say you’re bearish on $Monrock, a memecoin fresh off a launchpad, now trading on an AMM. By some miracle, it’s also listed on a lending market.

First, you deposit $1,000 USDC into the lending protocol. With a 50% LTV limit, you can borrow up to $500 worth of Monrock. You take that Monrock, sell it on the AMM for USDC, and now you owe Monrock back to the lender.

If the price drops, you buy back the same amount you borrowed, repay, and free up your collateral. If it rises, your collateral ratio shrinks. If the ratio shrinks too much, liquidators step in and liquidate your position.

Even if that sounds straightforward, in practice it almost never happens.

A token fresh out of launch rarely has a reliable price oracle, which means it won’t be listed on a lending market at all. Listing is a semi-permissioned process that requires governance or a risk team to approve it. And even then, you can only borrow if someone’s willing to deposit that same volatile token on the lending side, which for a thinly traded asset is rare.

Likwid’s solution

This is the gap Likwid sets out to close, which is to remove the need for two separate systems to trade and take leverage. If an AMM already has liquidity for a token, why not let that same pool power borrowing and lending too?

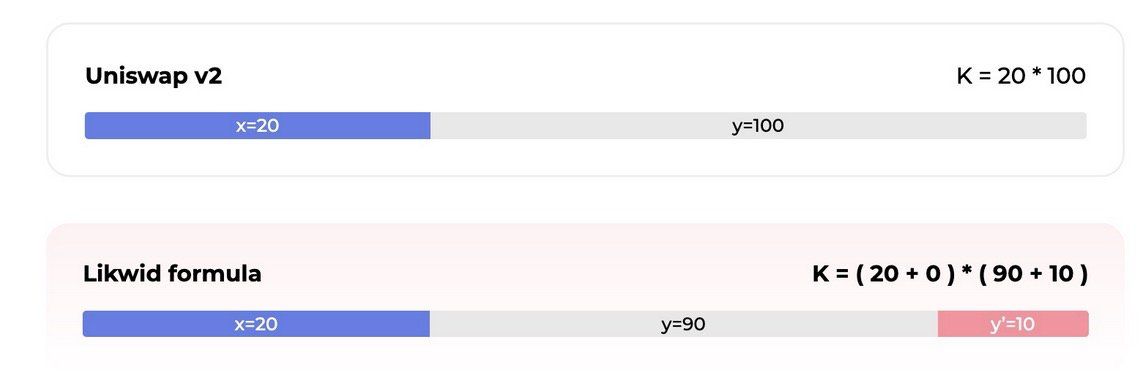

Likwid does this by through a novel constant-product AMM formula to account for two kinds of balances:

- the actual reserves in the pool, and

- “synthetic” reserves that represent borrowed amounts.

Think of these synthetic reserves as an internal ledger the pool uses to keep track of debt. When a trader borrows, the protocol mints synthetic tokens to represent what they owe. Those synthetic balances shift the curve in the same way real reserves would, so prices stay accurate without needing an external oracle to tell the pool where the market is.

In formula form, the pool no longer just keeps x × y=k for the real reserves x and y. It tracks both the real amounts and the synthetic amounts owed:

Here, x and y are the actual tokens in the pool, and x′ and y′ are the synthetic tokens that mark open debt positions.

By folding borrowing into the AMM itself, Likwid changes the workflow so that borrowing and swapping happen in the same pool atomically. If a token has a pool, it can be shorted or longed instantly, without an external oracle or waiting approval from a risk committee.

When you open a short on Likwid, you are borrowing directly from the AMM pool itself. And the pool keeps track of that debt with synthetic token.

Say you post token x as collateral and choose to short y. Under the hood, the pool’s contract mints an internal marker y′. You’ll never see y′ in your wallet and it is not something you can swap or send. The purpose of it is for the protocol to keep track of exactly how much y you owe.

Right after minting y’, the pool gives you real y from its reserves. You sell it instantly into the AMM curve. Now the pool has more y and less x, which nudges price of y upward. In other words, your short is impacting the market the moment you open it.

When you close your short, you must return the same amount of real y to burn the y’. Until then, the pool’s pricing automatically reflects your position, because both the real reserves and the synthetic debt are factored into the curve.

This design is what lets Likwid unify trading and borrowing in one place. The AMM itself becomes the lender, the borrower, and the execution venue. And the synthetic token is the bridge that makes it possible.

User flow

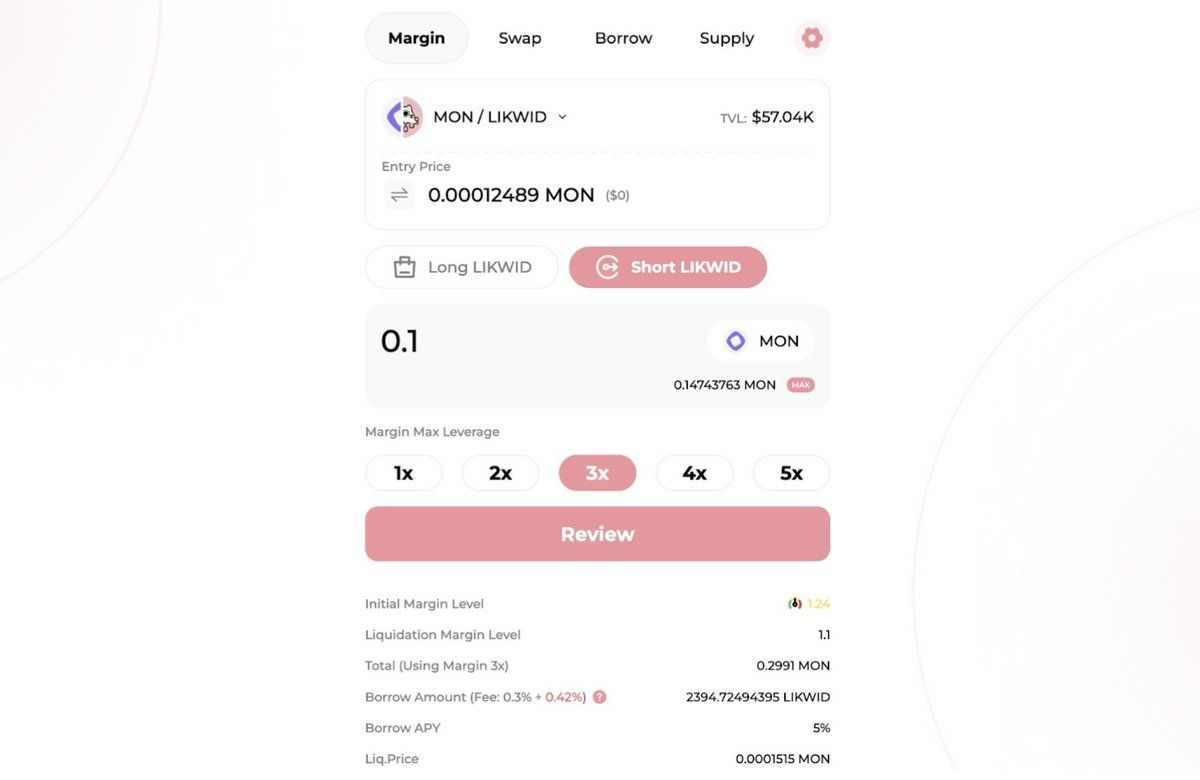

Let’s walk through a real example of how you would do this right now on Monad testnet.

From the top Navigation, you can choose your mode. In Margin, you’re taking leveraged long or short positions directly from the AMM pool. Swap is for regular spot trades, Borrow for taking assets out against collateral, and Supply for providing liquidity.

In this example, I’m interested in the MON/LIKWID pool pair. The UI tells me which token I’m going long or short on, and in what base/quote pair.

I will be attempting to short the LIKWID token while using MON token as collateral. In this case, I’m putting up 0.1 MON as my margin. The value below (0.14743763 MON) shows your max collateral based on wallet balance.

The leverage multiplier controls how much you borrow relative to your margin. At 3x, I’m using my 0.1 MON collateral to open a 0.2991 MON position.

At the bottom there are a list of relevant for my position tracking:

- Initial Margin Level (1.24) – A risk metric showing how far you are from liquidation. Higher is safer.

- Liquidation Margin Level (1.1) – If my margin level falls below this, my position gets liquidated.

- Total (Using Margin 3x) – Shows the total notional size of the position with leverage applied (0.2991 MON).

- Borrow Amount – The number of LIKWID tokens I'm borrowing, with fees broken out (0.3% fixed + 0.42% variable).

- Borrow APY (5%) – Annualized interest rate on the borrowed tokens.

- Liq. Price (0.0001515 MON) – The price of LIKWID at which your position will be liquidated if it moves against you.

Potential issues and mitigations

While Likwid’s design opens the door to more efficient, permissionless leverage, there are also potential pressure points.

1. Manipulation risk from short-term price spikes

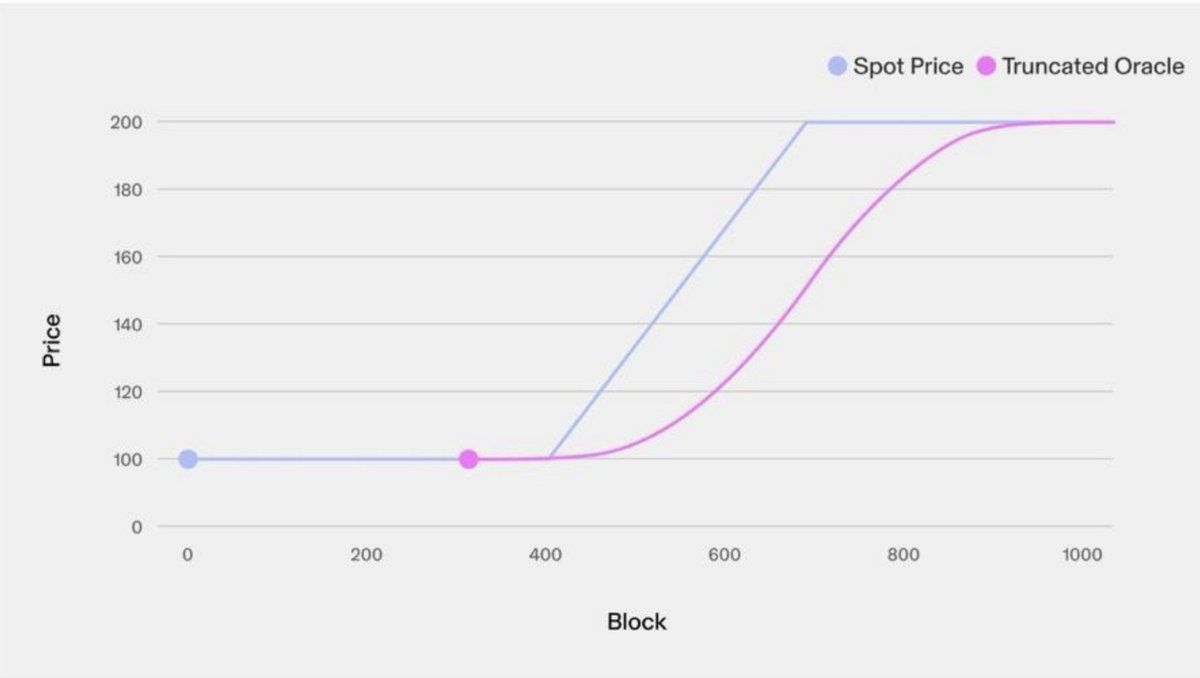

In most lending/derivatives protocols, liquidations depend on an external price feed. If the price feed tracks the market tick-for-tick, a manipulator can push the price sharply in their favor for a few seconds (e.g., with a big swap or flash loan) and trigger liquidations at that manipulated price. Profits can be extracted from liquidating healthy positions. Extreme short-term volatility can wrongly flag a position as underwater when it would be fine under a more stable price reference.

Likwid employs a truncated oracle which dampens the impact of extreme price moves by capping how much the reference price can move in one update, relative to the last known price.

This protects margin traders from being liquidated by single-block price spikes, either from manipulation or just random volatility. In leveraged trading, your position health is recalculated every block. If a big swap pushes the spot price sharply against you for even one block, you could get liquidated before the price snaps back.

2. Liquidity withdrawal risks

In AMMs + lending hybrids like Likwid, liquidity is the backbone. If too much liquidity leaves all at once, prices jump violently because there’s less depth to absorb trades. Positions that were fine at the old depth can suddenly go undercollateralized, triggering liquidations.

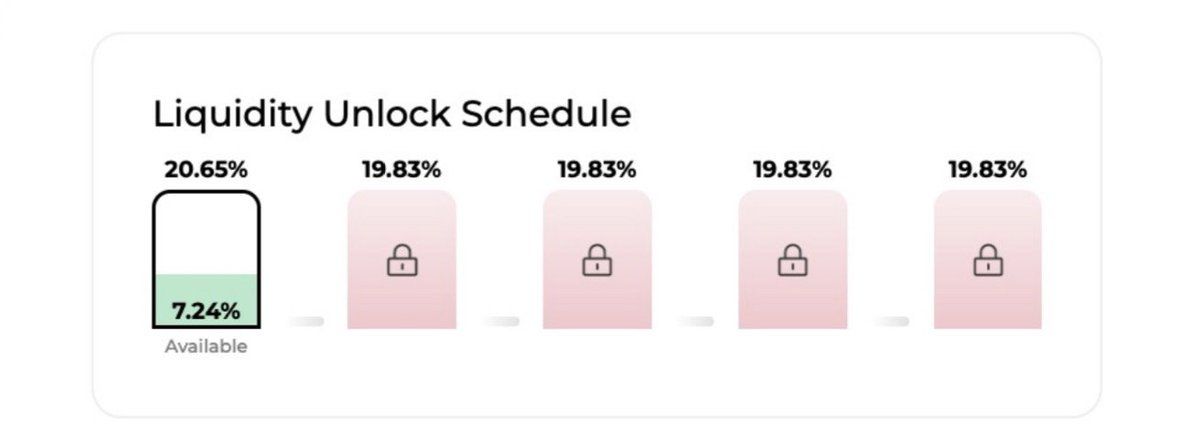

Likwid’s liquidity protection is designed to prevent that kind of “bank run”. Instead of letting anyone pull their entire position in one shot, the protocol releases liquidity in controlled cycles.

Liquidity can be withdrawn in fixed time cycles (e.g., every hour). Each cycle lets you take out a set quota of your position, or your “base unlock.” If exit pressure stays low, you keep getting the normal quota each cycle. If exit pressure spikes. meaning lots of other LPs are trying to leave, the next cycle’s quota automatically tightens, slowing the drain for everyone.

The system doesn’t lock users indefinitely or require governance to flip a switch. It just smooths exits across time, buying the protocol room to breathe during volatility. In calm markets, this should be barely noticeable. In stressed markets, this would be the circuit breaker that keeps liquidity from vanishing in a single block.

Why this matters

By merging AMM liquidity and lending into one pool, Likwid unlocks leverage for any token with a market, removes the oracle bottleneck, and removes the friction of hopping around multiple protocols. What this means is that:

- Newly launched or long-tail tokens can be longed or shorted instantly, without waiting for a lending market to list them.

- In theory this should lead to better price discovery as overvalued assets can be bet against early.

- Other protocols can tap into Likwid’s unified pools without inheriting the risk of fragile price feeds or off-chain liquidators.

But adoption won’t be automatic. Real questions remain:

- Can traders realistically put on size without blowing through pool depth and eating massive slippage?

- Can Likwid win in long-tail markets where volatility is already extreme without leverage?

- Will LPs actually earn enough to justify the extra exposure from the lending component. Or will that added risk keep them from committing meaningful capital?

- Will LPs accept the withdrawal schedule limits and lock-up mechanics, or will those constraints make capital sticky in ways they don’t like?

Likwid's value prop is built on the sensible assumption that traders will trade more if the rails are seamless, and that LPs will supply deeper pools if the returns justify the risk. If that bet pays off, every token will be a two-way market from day one and people can finally stop asking the question “hey, where can I short this?”