What’s Next for Interactive Entertainment

- Published on

- · 9 min read

Have thoughts on this topic? Join the conversation on X

The next generation of interactive entertainment applications will be very different to what we’ve been accustomed to. Just look at what’s being vibe coded and you’ll see that creativity is evolving from content into applications.

Interactive entertainment is now an amalgamation of games, user-generated content (and apps), and social networks. Apps and economies built around these elements now compete with social media platforms for screentime.

Onchain interactive entertainment will proliferate in the next decade by turning skill, risk, ownership, and incentives into composable primitives that create novel, social, and tradable experiences.

- Attention is scarce in a sea of alternatives

- State of interactive entertainment

- The attention barbell

- What’s next then?

- Final word

Attention is scarce in a sea of alternatives

People these days are juggling apps more than ever. Adults use an average of 41 apps per month, and the global average person uses 7 social platforms per month. More places to go on your screen means the lower switching cost. Don’t like an app? Just swipe up and go to another. Retention is extremely difficult for anything that isn’t a default habit.

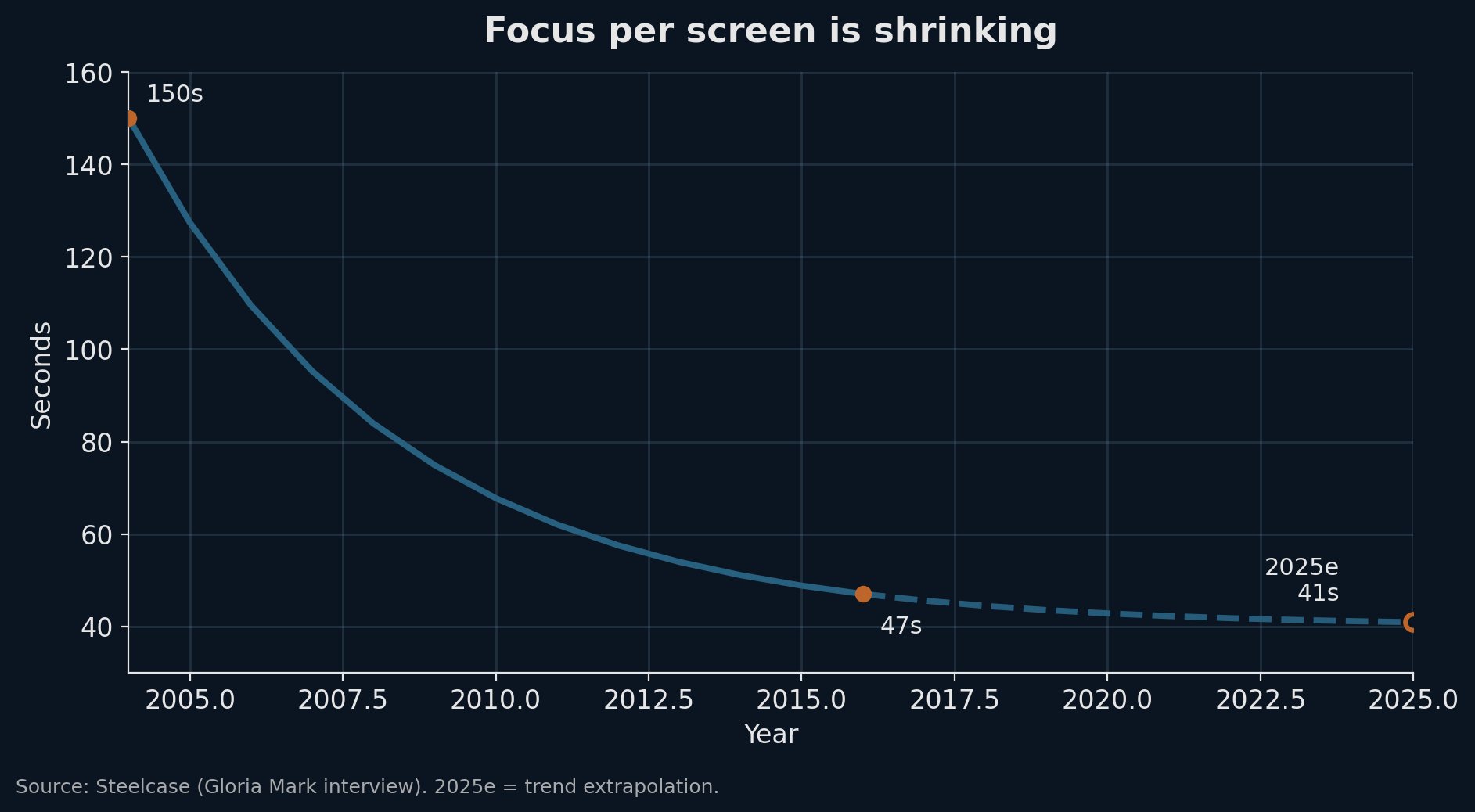

UCI’s research showed that in the early 2000s the average time people stayed on a single screen was 2.5 minutes. Today, it is less than 47 seconds. What this means is with an abundance of alternatives, discovery matters a lot. Content comes to you, and you don’t “decide” to seek it.

State of interactive entertainment

Interactive entertainment, specifically gaming, is starting to compete on the same realm of novelty, discovery, and social networks as other apps. Social media platforms have siphoned away a lot of attention from gaming experiences, resulting in the case that any game that’s not hypercasual or has a deep lore has low retention.

The competition now simply isn’t just having a better game session than another game, but having a more engaging screen session than another app given the fixed attention budget that people have.

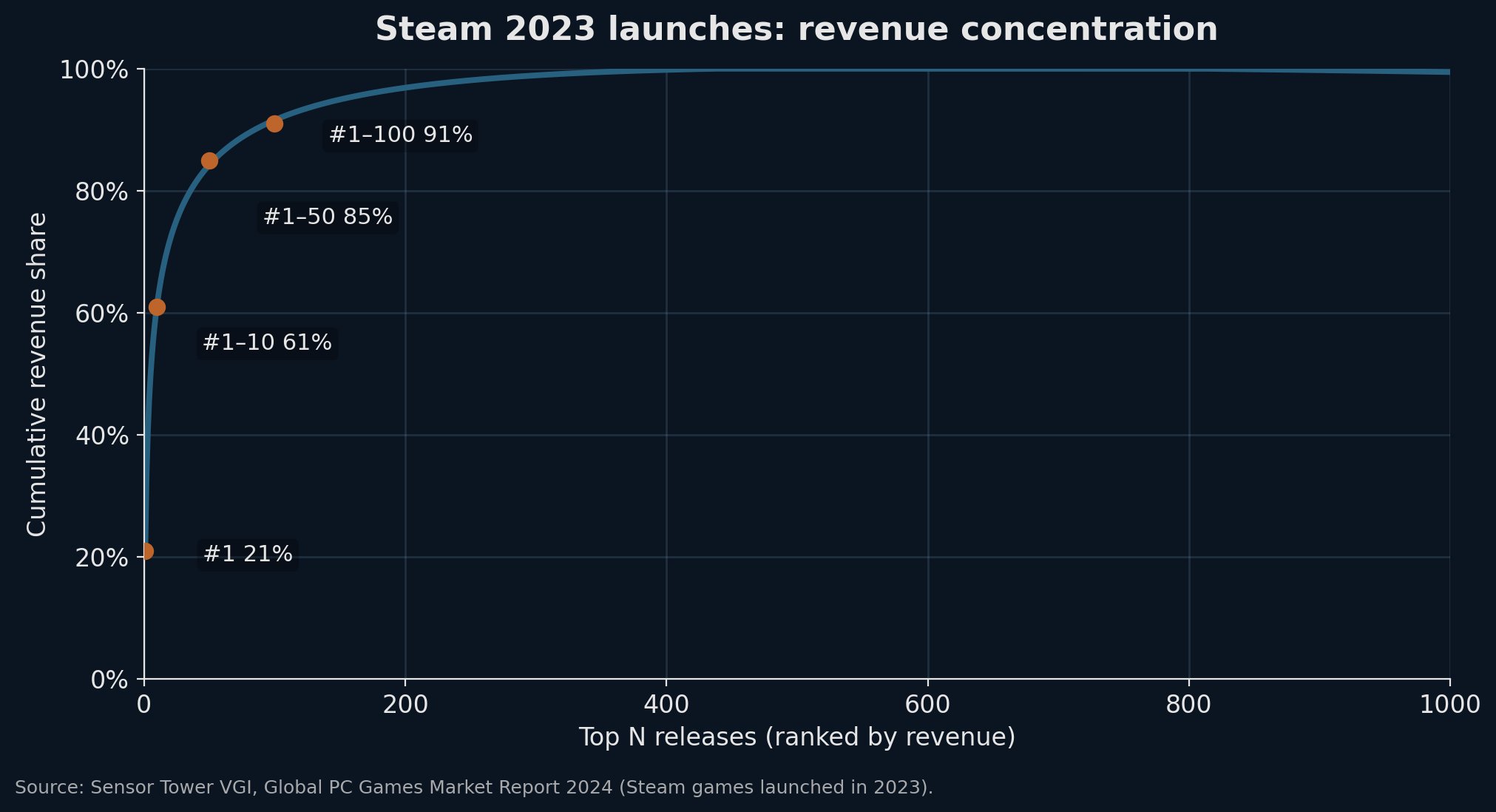

Just look at the thousands of annual game releases now fighting for 12% of playtime. The top game gets 20% of sales and top 1-10 take 60% of sales. From a profitability perspective, VCs have taken their allocations elsewhere, studios have shut down, and game-maker stocks have underperformed.

What this means is that users will continue to play the Fortnite and Apex Legends of the world (with the addition of ARC Raiders) and generally stick to trying one or two big releases on Steam.

The paradox is that the gaming market is enormous at a TAM of ~$200bn, but growth and profit are concentrating in the top few.

Matthew Ball summarizes it well:

The exhaustion of decade-plus growth drivers that grew players, playtime, and spend… coincided with evolving user behaviors, changing monetization models, and growing ‘lock-in’ effects… that exacerbated long-running competitive and budgetary escalations… while growth concentrated in foreign markets that shifted to local productions (and then took share abroad)… and occurred alongside acute macroeconomic financial events and epidemics… were worsened by microeconomic platform policy shifts… as well as the emergence of new and hyper-viral substitutes… and foreign-based competition… alongside too many would-be new growth drivers that have yet to deliver growth.

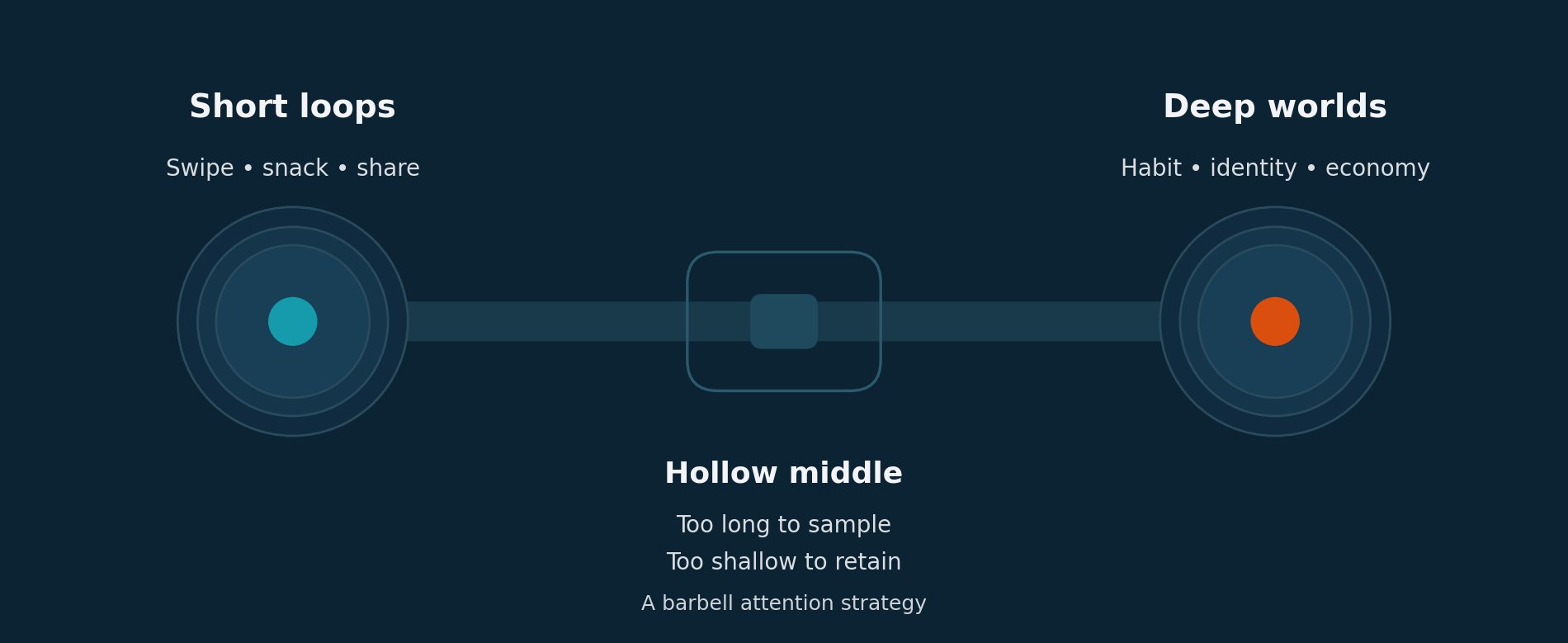

The attention barbell

Applications now fall on a barbell. One end is short, high-frequency loops like scrolling through TikTok or hypercasual games. Mobile “short-loop” experiences have strong cash flow: Monopoly GO passed $2bn lifetime revenue 10 months after launch. The other is deep, high-retention experiences like MMOs. Epic Games paid out $352mm to creators in 2024 and Roblox has paid $3.3bn to creators since 2018.

Anything in the middle is difficult to retain users since it’s not developed enough to become a habit but not short enough to capture a moment’s attention and quick dopamine hit. The market for attention is saturated, and feeds are optimized for constant context switching. This means that anything “mid-length” is hard to retain because it’s not instantly gratifying but also not a daily habit.

Interactive entertainment competes on the same feed-driven attention economy - games aren’t just competing with games. They’re competing with TikTok, YouTube, Netflix, and Spotify for slices of the same attention pie.

As AI tools proliferate, it becomes easier and easier for applications to be made. In a world where you can build anything, discovery becomes the moat. Anyone can build, but not everyone can tell a real story. The builders who win likely won’t just be the best engineers but the ones who capture attention with something authentic and relatable.

What’s next then?

2026 is the inflection point for interactive entertainment with 3 converging forces:

- AI tooling getting close to production quality

- Distribution becomes important as creator monetization hits fee ceilings

- Onchain infra reaching Web 2.0 UX parity

AI

There seems to be a disgust towards the use of AI for game development so far as to disqualify games for doing so.

But franchises that used to spend $50 million per title 15 years ago now spend $200 to $500 million today to develop per Sony. These new AI tools will significantly decrease development cost over time. Yes, the use of generative AI is not an excuse for sloppiness. Studios should still be held to a high standard for quality and experience.

A few months ago nobody even thought of vibe coding games. Now people are experimenting everyday:

And AI enables incredible experiences - look at MIMESIS, a co-op survival horror where AI mimics teammates’ voices and actions to create paranoia.

AI will start to commoditize the product layer, and a defensible moat will then become discovery: authentic stories that make people want to participate.

Distribution and discovery

Distribution is more important than ever as the number of applications hitting the app store and the web in general will skyrocket. And creators will lead this next wave of adoption.

Why are so many companies hiring storytellers? Because stories will drive the next wave of discovery as “slop” hits the market. Stories make these applications feel real and relatable, and creators will amplify good stories.

Take Sledding Game for example, an upcoming multiplayer sandbox game focused on chaotic, physics-based sledding with friends.

Sledding Game built a story around a recognizable creator persona (sled guy), a cast of cute animal avatars, and heavy social elements (friend in the game playing roulette betting all on red and losing it all). Fans recognized and could understand in a few seconds through Instagram Reels, and audience reactions influenced what became real in the game.

The social identity translated into a cozy Steam product built for clip-generation. The game has over 200,000 wishlists on Steam currently.

Sledding Game isn’t an exception. Among Us launched in 2018 and was ignored for two years. Streamers and creators discovered it in 2020, and turned the indie game into a cultural phenomenon.

Onchain applications

Web3 consumer apps have had controversial reputations historically, but with the combination of AI and discovery, will evolve into onchain interactive entertainment experiences that allow teams to monetize quickly.

There are very exciting areas to explore:

- Internet Money Gaming: platforms that facilitate skill-based risk-to-earn interfaces where players can wager on their own outcomes. This effectively captures the adrenaline and engagement of esports but on an atomic and micro level, allowing thousands of competitions to be run.

- AI-enabled Games: build with AI, monetize onchain, and have rails that are ready for a global audience since day 1. Provenance protocols let creators prove what they made and earn when others expand upon them.

- Gamified Financial Micro-Experiences: unbundled financial "micro-experiences" that simplify complex derivatives and yield strategies into sticky, dopamine-driven loops.

- Gamified Utility: apps that gamify necessity, transforming daily routine actions into entertainment.

- Autonomous Worlds: hybrid to onchain games where the world state is permanent and composable. Players and AI agents can build on the world and extend it permissionlessly.

Onchain apps will find PMF on both ends of the barbell:

- Short-loop, high-frequency: gamified finance, internet money gaming, where the dopamine comes from financialization

- Deep, high-retention: autonomous worlds, gamified utility with achievements, worlds built with AI

Moreover, teams building onchain need to tell a compelling story about the experience they are curating. When users own a piece of what you’re building, they become your distribution. And effective distribution needs a good story.

Final word

Interactive entertainment will look quite different in a year from now, and that’s extremely exciting. The breakout experience in the coming years won’t just come from the best engineers or biggest budget. It’ll come from someone with an audience and a real story - built with AI, monetized onchain, and distributed authentically.

Onchain applications will need to take lessons from existing viral applications primarily when it comes to distribution and onboarding. Tell a story about your app that makes people relate and want to try it. Discovery is still off-chain, so onchain teams need to tap into that audience. But once a user decides to participate, teams must remove onboarding friction so they can try it in less than a minute, because every click and tap that isn’t fun increases your risk of churn.

AI will accelerate a cambrian explosion of apps, and adoption for onchain apps will not come from asking users to be crypto-native, but from users chasing the best experience, wherever it lives.

If you’re building in this space, please reach out to @G_G_M_F and @charlxvii