Merchant PSPs: The Boring Case for Stablecoins

Harry Alford

@HarryAlford3 (opens in new tab)- Published on

- · 5 min read

When people think about payments infrastructure, they usually think of global platforms like PayPal, Stripe or Adyen. But in Southeast Asia, Africa, and Latin America, the real volume moves through a layer most people never notice: merchant payment service providers (PSP).

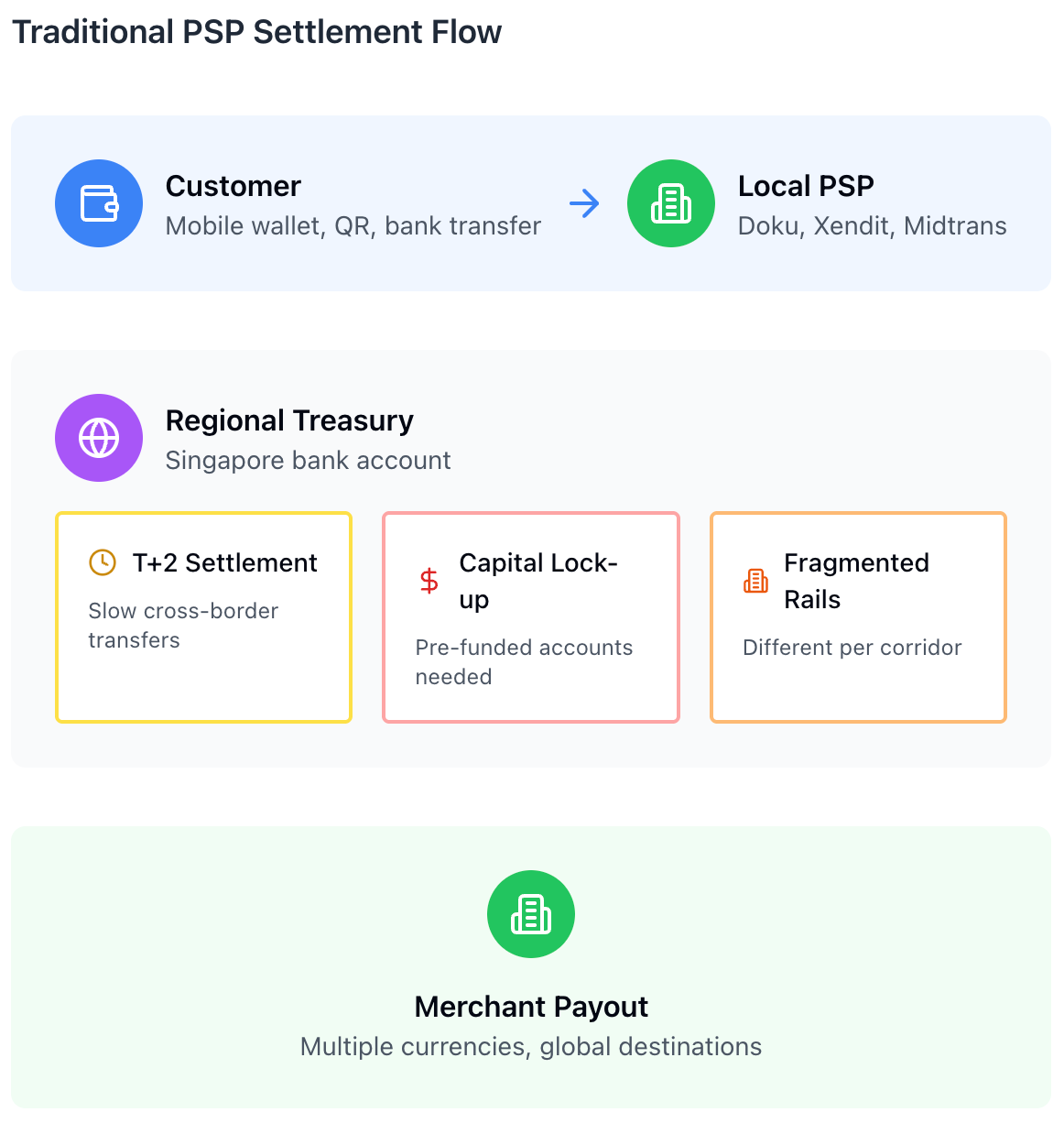

Merchant PSPs are local payment gateways that help merchants accept alternative payment methods beyond cash and cards, such as mobile wallets, QR payments, bank transfers, and local debit schemes. Because payments are regulated locally, PSPs typically require local licenses and banking relationships in each market in which they operate. Examples include Indonesia-based PSPs like Doku, Xendit, and Midtrans, as well as the Philippines’ DragonPay.

Domestically, these systems work. Countries have invested heavily in real-time payment infrastructure, and local settlement is increasingly fast and cheap. The problem starts at the border. The moment a PSP needs to pool funds across markets, convert currencies, and pay out merchants or platforms regionally, they face slow correspondent banking rails, pre-funded nostro accounts, and manual treasury operations that haven’t changed in decades. And this is where stablecoins have the most credible promise.

The Core Pain: Settlement and Working Capital

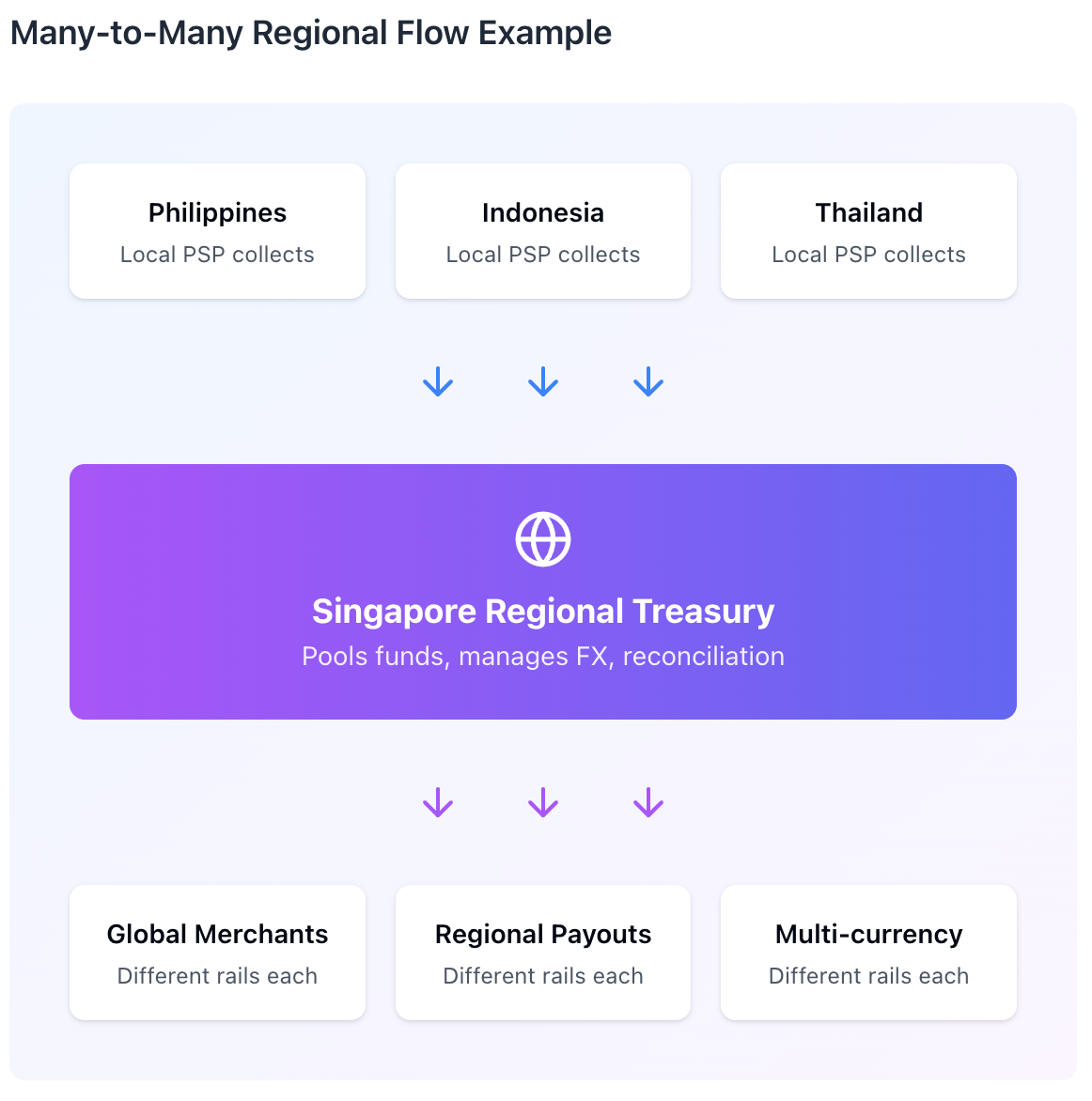

PSPs collect locally but settle regionally. A Philippine-based gateway might aggregate payments from GCash, GrabPay, and local bank transfers in Manila, pool those funds into a Singapore hub account, convert to USD, and distribute payouts to merchants across multiple countries. This flow touches three or four banking relationships, at least two FX conversations, and multiple regulatory jurisdictions. The various cutoff times, compliance requirements, and settlement windows increase operational complexity.

The primary cost of this flow exceeds transaction fees at each step. It's in capital efficiency.

To keep settlement flowing across, say, five Southeast Asian markets, a mid-sized PSP might need to pre-fund millions of dollars in nostro accounts across currencies just to manage timing mismatches. For instance, the PHP-to-SGD-to-USD corridor may take three days to clear, whereas merchants expect T+1 or faster payouts. When volumes spike during a regional sale event or holiday period, treasury teams are scrambling to manually move liquidity between accounts, often racing against bank cutoff windows that vary by market and correspondent bank.

This is worth being precise about because it defines what any alternative settlement rail must solve. The ‘pain’ is a result of the interactions between slow settlement, fragmented banking infrastructure, and the capital inefficiency that results. A solution that speeds up one leg but doesn’t reduce pre-funding requirements or simplify reconciliation won’t meaningfully change the economics.

Why Stablecoins Are Attractive and Hard

Stablecoins offer near-instant settlement, 24/7 availability, and unified liquidity across borders, exactly what PSP treasuries want. For example, dLocal began using USDC as an intermediary settlement layer in 2025, reducing settlement times on certain corridors. The use case is real, but adoption is constrained by institutional barriers:

- Bank restrictions: Most partner banks prohibit crypto from being used in regulated fund flows. In practice, this means PSPs can't simply convert collected fiat into stablecoins within the same entity and banking structure they use for licensed payment processing.

- Treasury change management: New custody models, policies, compliance processes, and internal approvals take time to implement.

- Cost sensitivity: The total on/off ramp cost needs to land around 1-3 bps to beat correspondent banking. On thinner corridors, the on/off-ramp spread alone can eat the savings.

- Merchant accounting risk: If merchants receive stablecoins directly, they may be required to hold and report crypto on their balance sheets, which most seek to avoid.

As a result, most PSPs prefer models in which merchants remain fiat-native, with stablecoins operating behind the scenes in settlement and treasury workflows.

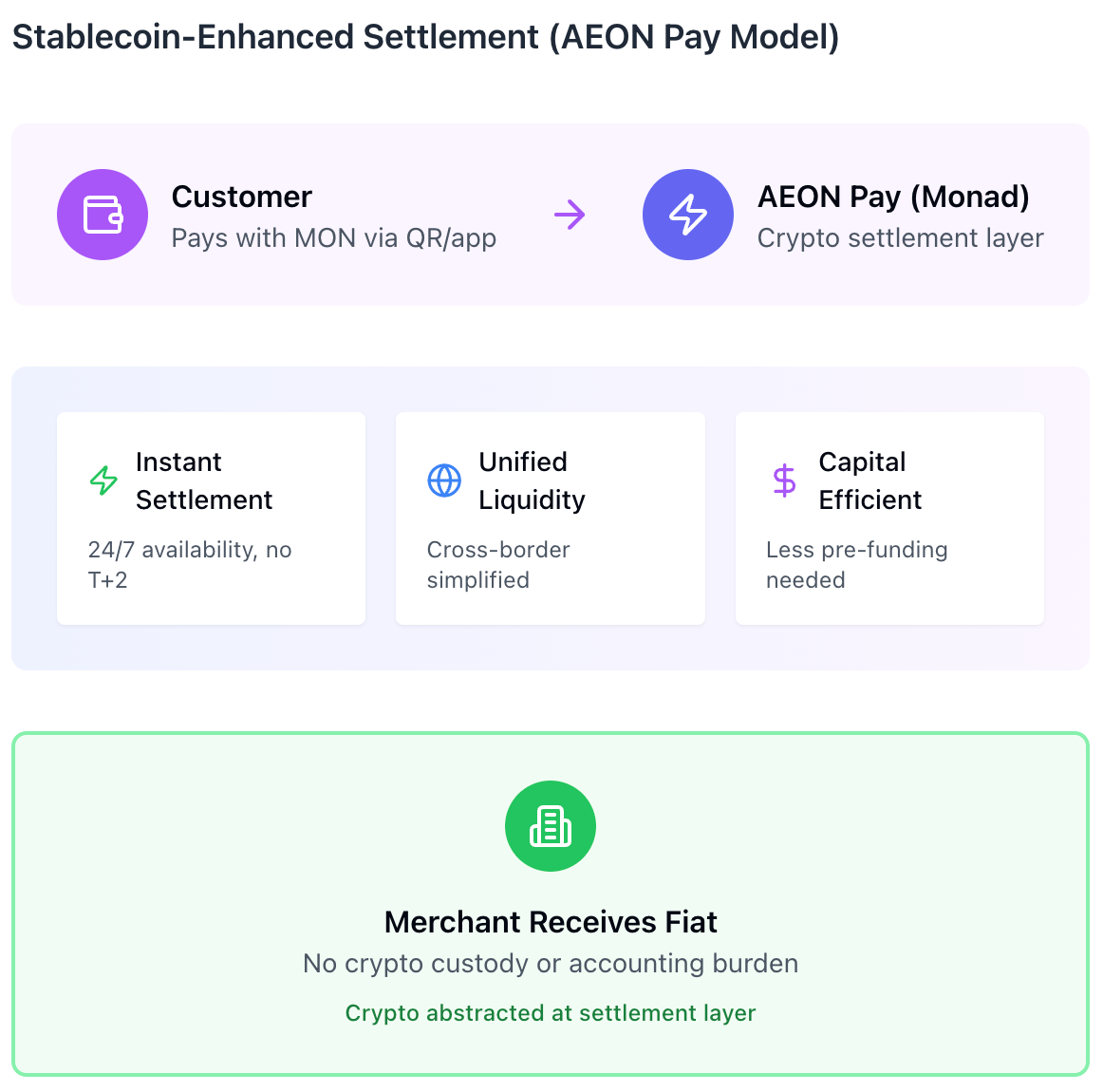

A Real-World Example: AEON Pay on Monad

AEON Pay, now live on Monad, shows what this can look like in practice.

AEON Pay enables crypto payments to 50+ million merchants worldwide via QR codes and bank transfer rails across Southeast Asia, Africa, and Latin America. With Monad integration, users can now pay with MON online and offline through AEON’s mobile app and wallet integrations.

Critically, merchants receive fiat. They don’t custody crypto, don’t report it on their balance sheets, and don’t change their existing payment acceptance workflows. The crypto-to-fiat conversion occurs at the settlement layer, abstracted away from the merchant.

Why This Matters

Merchant PSPs are a relatively new yet critical layer of the global payments stack. They move massive real-world volume but still operate on slow, fragmented settlement rails.

Stablecoins offer a genuine technical improvement for parts of this problem. Settlement speed drops from days to minutes, pre-funding requirements shrink, and treasury teams gain 24/7 optionality that traditional rails can’t provide.

But while stablecoins solve the technical problem of moving value, they don’t solve the institutional one. Fiat-on/off ramps remain necessary at both ends, and adoption is constrained by banking relationships, regulation, and treasury workflows. As a result, stablecoins deliver the most leverage in corridors where traditional rails are weakest, emerging markets to emerging markets, and thin corridors with limited banking coverage.

If stablecoins can integrate seamlessly into PSP treasury workflows without disrupting banks or merchants, they enable faster settlement, improved capital efficiency, and more scalable cross-border commerce. Not by replacing PSPs, but by quietly upgrading the rails underneath them.